The Kennedy Report Exclusive: An In depth Review of COunty Finances for Previous and Current Years Spending

An Accounting of County Funds and Expenditures

Written by

Kathryn Kennedy, MBA, CPA (Inactive)

Lorain, Ohio

Financial columnist for The Kennedy Report

Part #1 – Analysis of Funding/Spending

It appears that General Fund dollars would be sufficient to fund the Sheriff’s office – but the county commissioners are looking to use the $13.9 million from the Midway Mall sale – and of a portion of the $20 million that was set aside for the jail to provide matching funds for the proposed mega-site development at the Lorain County Airport. (Noted in newspaper articles where Dave Moore was quoted).

Why wouldn’t the commissioners just state – we are proposing the sales tax increase so we can use General Funds for other projects?

Once those one-time funds are used for matching the mega-site funding – then, what will those funds be used for going forward?

The answer – partially to fund the increased spending that has occurred over the past few years – including large, ongoing wage/salary increases.

Analysis of funding/spending:

County commissioners make decisions and news outlets report them – that narrative is reflected in the audited financial statements. Let’s see if they match…….

In 2016, the ¼ of 1% increase in sales tax was voted down. In 2017, the county commissioners – Kalo and Kokoski – voted it in. Lundy abstained.

Reason given for the vote – “the county was facing a 35% budget cut – and would have hit the sheriff’s office hard.”

Where did the 35% come from – as that would have been a cut of $20 million…..expenses actually decreased $1 million from 2016 to 2017.

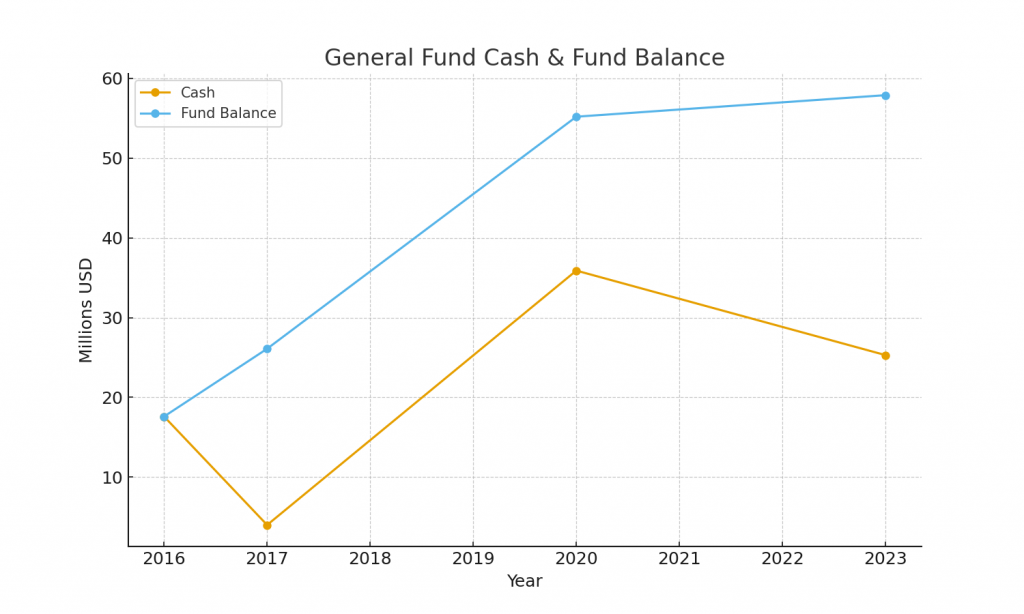

At the end of 2016, the county had a General Fund fund balance of $17.6 million. (Fund balance means excess revenues over expenses over time. The larger the number, the more financially secure).

At the end of 2017, the county had $4 million in cash (this number changes constantly based on cash coming in and going out). The fund balance increased to $26.1 million.

Revenues (property taxes, sales tax, fees, etc.) were $13 million ($6 million of that was an increase in the sales tax) more than expenses in 2017. Even without the sales tax increase – there were funds to cover expenses.

By the end of 2020, the county General Fund had $35.9 million in cash and the fund balance had increased to $55.2 million – an increase of $37.6 million since 2016. Revenues in 2020 were $21.4 million greater than expenses.

The commissioners may have had a reason for increasing the sales tax in 2017 – but it doesn’t appear it was for the stated reason. Did they not realize there was such a build-up in the fund balance over time?

Was funding the sheriff’s office given as a reason – and then there were other plans for the excess funds being collected?

And, why would the county auditor not bring this excess funding to light?

In 2020, Sweda, Lundy and Kokoski voted to rescind the sales tax increase from 2017.

Fast forward to 2023 (the most recent audited financial statements) – cash totals $25.3 million, the fund balance is very strong at $57.9 million – and revenues are greater than expenses by $20.3 million.

It doesn’t appear – at that time (2023) – that a sales tax was needed. Audited financial statements are not yet out for 2024.

The commissioners are now asking for a new 1/4 of 1% to fund the sheriff’s office and jail operations. The sales tax increase is expected to bring in about $13 million a year.

The sheriff and jail operations budget for 2026 is 14% greater than 2025 – increasing to $35.5 million – so if the sales tax passes, about $10 million from the General Fund would still be required to fully fund jail operations and the sheriff’s office.

In 2025 – and prior years – 100% of the sheriff’s budget came from the General Fund.

$20 million from the General Fund was set aside (December 2022) to fund future jail construction and a $13.9 million loan (January 2023) was made to the Lorain County Port Authority to purchase the Midway Mall – in anticipation of selling it. That deal has yet to close.

Even with these decisions, is it possible that the $57.9 million fund balance at the end of 2023 was depleted by that much in 2024 – and 2025 to date – that there is a general fund budget deficit?

Edit:

In effect the over-collection of General Fund sales tax from 2017 to 2020 allowed the $20 million to be set aside for the jail and the $13.9 million for the mall purchase.

The recent disclosure of the mega-site to be developed in New Russia Township requires about $22 million in local matching funds. Moore stated the matching funds would not be an issue…..He said – the $20 million previously set aside for the jail and the expected receipt of the $13.9 million plus interest for the sale of the mall could be used for matching funds.

So, in effect, the county DOES have the funds for the sheriff’s office and jail operations – but it appears they want to use General Fund dollars for the mega-site development. Why not just say that?

When asked to approve a sales tax increase – or any tax increase, we should, at the very least, get accurate and full information – in order to make an informed decision.

Two more posts to follow – one on how the $60 million in ARPA (American Rescue Plan Act) – funds were spent – and detail on county spending, including county salaries and wages.

Questions, please ask. Photos to support the data (Ohio Auditor website) and comments of commissioners (Chronicle).

Edit:

I did attempt to discuss this with the sitting commissioners prior to this post.

Part #2 – ARPA Funds & Spending

Updating to add information from a records request. Numbers for the General Fund from the Tax Budget (since 2024 audited financials not yet available).

Cash balances remain strong – but spending is outpacing receipts.

2024 Actual:

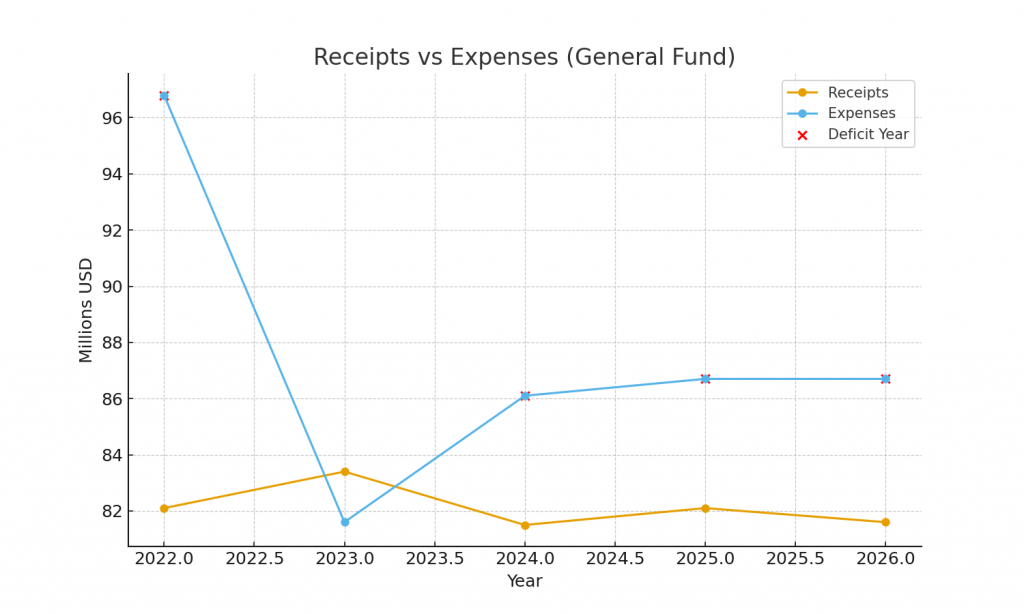

Cash, $23.1 million. Receipts, $81.5 million. Expenses, $86.2 million.

2025 Projected:

Cash, $18.5 million. Receipts, $82.1 million. Expenses, $86.7 million.

2026 Estimated:

Cash, $13.8 million. Receipts, $81.6 million. Expenses, $86.7 million.

Deficit spending since 2024.

Of note, in 2022 –

Cash, $36 million. Receipts, $82.1 million. Expenses, $96.8 million.

Part #2

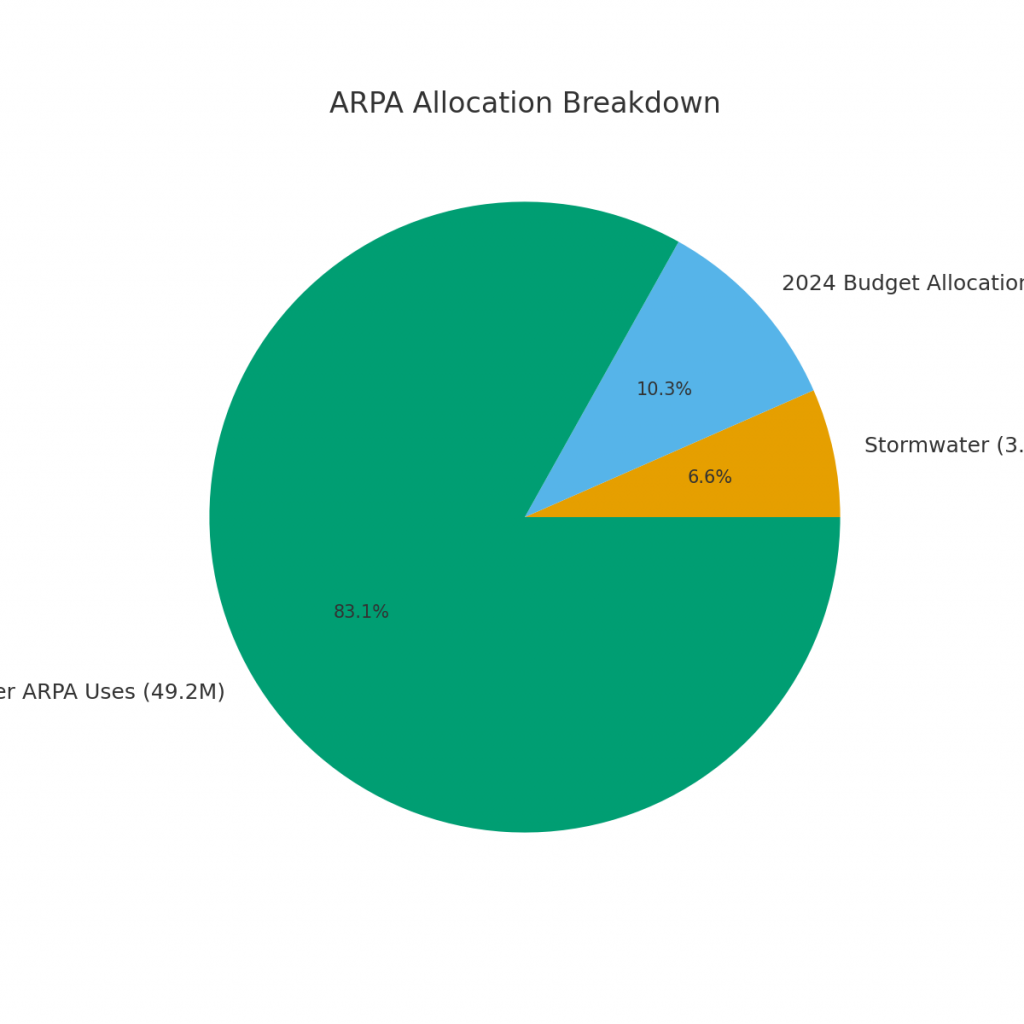

The county received $59.2 million in ARPA (American Rescue Plan Act) funds. (From a records request to the county auditor’s office).

Funds are reflected in the 2022 and 2023 audited financial statements.

Funds needed to be obligated (decision made) by December 31, 2024 and spent by December 31, 2026.

A standard allowance of up to $10 million of these funds was allowed for water/sewer, roads/bridges.

Confirmed that $3.9 million of the ARPA funds was directed to stormwater, ditch and sewer projects. None was directed to roads/bridges.

County commissioners increased the vehicle registration fee by $5 in May 2025 to fund road and bridge improvements. This increase will bring in about $1.4 million, annually.

Greene County (Ohio) used $10 million in ARPA funds to fund jail construction along with a $15 million grant from the state. (Other funding for the $75 million project – $20 million in General Fund cash and $30 million in sales tax-funded bonds).

Lorain County set aside $20 million from the General Fund for jail construction in December 2022. $1.7 million of that amount was approved for jail design in July 2025.

In the 2024 budget, the commissioners used about $6.1 million in remaining American Rescue Plan Act (ARPA) funds to provide all county departments with their requested funding – with no budget hearings.

Edited to add:

Looking at the tax budget for 2024 through estimated 2026, expenses are running about $5 million above receipts.

It appears the county commissioners used one-time ARPA funds to increase expenses long-term, starting with that 2024 budget giveaway (reported $6.1 million).

Why weren’t ARPA funds used for more long-term projects?

Why weren’t ARPA funds used for longterm purposes – e.g. roads/bridges, jail construction (If planning had proceeded to get it done by 2026).

Instead, ARPA funds largely went to payroll increases, etc. – that are continuing expenses with no corresponding revenue increases going forward.

It appears the county needed to off-load some expenses to cover the increased spending – including the proposed sales tax, the $5 vehicle registration fee – and just recently increasing the healthcare premium employee payment.

Note: Attempted to discuss with commissioners – to find out their reasoning on spending – prior to posting this.

Part #3 – Tax Budget, Wages, and Long-Term Spending

The county Tax Budget (obtained by records request to the county Auditor), shows the following receipts and expenses for the General Fund, respectively:

2022: $82.1 million / $96.8 million

2023: $83.4 million / $81.6 million

2024: $81.5 million / $86.1 million

2025: $82.1 million / $86.7 million

2026: $81.6 million / $86.7 million

Although not audited financial statements, this tax budget was provided as current (2024, 2025 and 2026) audited information would clearly not yet be available. It does provide comparison for the years presented.

Expenses have outpaced receipts since 2024.

It appears the budget give-away of 2024 (with ARPA funds of about $6.1 million) may have created that increase in expenses; pairing ongoing expenses with a one-time ARPA payment.

The largest expense for the county is salaries and wages.

A records request from the county Auditor shows the following (not broken out for General Fund, only, but for the entire county):

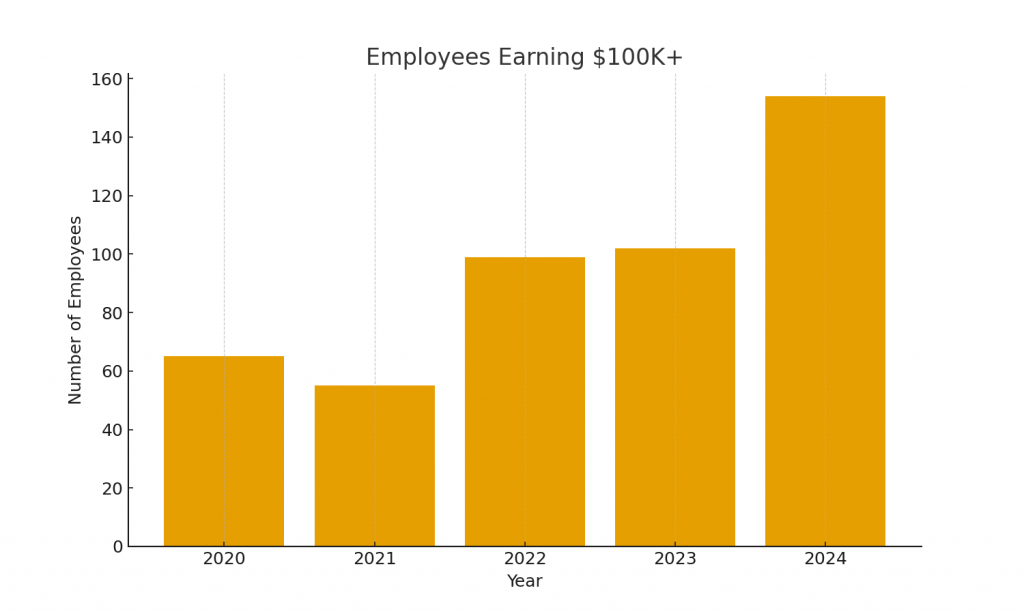

Number of employees earning $100,000 and over:

2020 – 65 at $8.1 million total – (increased dollars in 2020 over 2021 likely due to the $5 million in approved COVID-hazard pay)

2021 – 55 at $6.4 million

2022 – 99 at $11.4 million

2023 – 102 at $11.6 million

2024 – 154 at $17.2 million

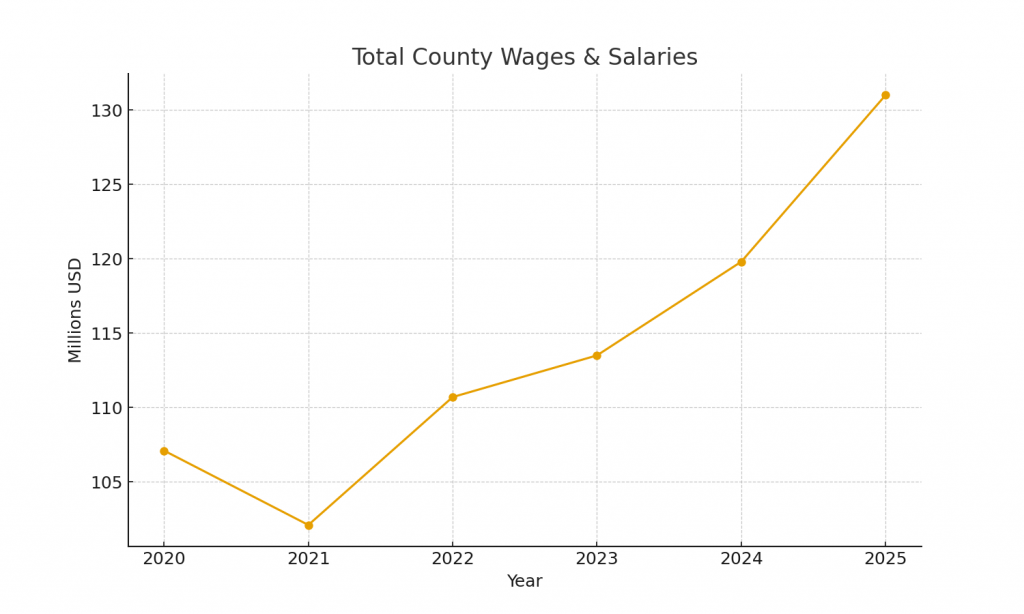

Total county wages/salaries:

2020 – $107.1 million (increased by $5 million in approved COVID-hazard pay)

2021 – $102.1 million

2022 – $110.7 million, increase of 8.4 percent over 2021

2023 – $113.5 million, increase of 2.6 percent over 2022

2024 – $119.8 million, increase of 5.5 percent over 2023

2025 – $131 million (estimated), increase of 9.3 percent over 2024 (budgeted)

It appears the budget issues may be directly attributed to the large increases in wages/salaries.

In the private sector, wages typically increase about 2 percent, annually.

It appears the county commissioners increased the vehicle registration fee ($1.4 million expected, annually) and hope to move the approximate $13 million funding for the sheriff’s office to relieve the pressure on the General Fund – both to cover the increased expenses – and to fund economic development (mega-site), etc.

On July 22, 2025, Moore stated they were reviewing twelve areas where the budget could be cut (at end of the sales tax hearing video on you-tube).

Curious this wasn’t done BEFORE the sales tax was placed on the ballot.

Wondering where the commissioners are on the budget – and what savings have been achieved to date.

County commissioners in place:

2019 – Kalo, Lundy, Kokoski. (Kalo replaced by Sweda in February)

2020 – Lundy, Kokoski, Sweda

2021 to 2022 – Lundy, Hung, Moore

2023 to 2024 – Riddell, Moore, Hung

2025 – Riddell, Moore, Gallagher

Submitted this to Letters to the Editor – Morning Journal and Chronicle Telegram on October 14, 2025.

2023 Lorain County audited financial statements report strong cash and General Fund balances.

The Tax Budget through 2026 reports continued strong, but declining balances.

Spending cuts in twelve areas mentioned at a July 2025 sales tax hearing remain unknown.

Excess General Fund dollars collected from the 2017 to 2020 sales tax increase allowed the setaside of $20 million for future jail construction and $13.9 million that was loaned to the Port Authority to facilitate the Midway Mall sale.

Commissioner Moore notes that matching funds for the development of the mega-site at the Lorain County Airport will not be a problem.

The $13.9 million from the mall sale, when finalized and returned to the General Fund, is roughly equivalent to the funds that would be raised by the proposed sales tax increase.

In 2024, remaining ARPA funds were used to provide whatever was requested by county departments, including substantial wage increases – with an expected 9.3 percent increase from 2024 to 2025 – outpacing an average 2.5 percent in the private sector.

Using one-time funds to cover continuing expenses is never advisable and contribute to the expected budget deficit for 2026.

If the $13.9 million from the mall sale can be used to match funds for mega-site development, those same funds might be used to fund the Sheriff’s office.

The county should then follow-through on spending cuts to provide a balanced budget and mega-site matching funds to also include cash balances and a portion of the jail construction funding, if needed.

Full disclosure of all expected county spending is required for voters to make an informed decision on the proposed sales tax increase.

AI Chart Disclaimer

Note: All charts included in this report were generated by Aaron Knapp using AI-based visualization tools. These visuals were added solely for clarity and reader understanding. Kathryn Kennedy did not create, edit, or supply any charts, graphics, or visual materials associated with this analysis. Her contribution consists exclusively of her written financial review and commentary.