They Knew. They Approved It. They Couldn’t Prove It.

Inside the Lorain Payroll Investigation That Found Problems Everywhere—and Accountability Nowhere

Aaron Knapp

Lorain Politics Unplugged | Knapp Unplugged Media LLC

I. INTRODUCTION — A CASE THAT NEVER WENT AWAY

There are cases that collapse because nothing happened, and then there are cases that collapse because too much happened inside a system that was never designed to produce clean answers. What unfolded inside the City of Lorain’s payroll structure falls squarely into the second category, and that distinction is not theoretical. It is the dividing line between a system that functions properly and one that cannot be held accountable even when the underlying conduct is documented, questioned, and escalated through multiple levels of government.

From the outset, this was never treated as a routine internal matter. Karen Shawver did not quietly note a discrepancy and move on. She documented what she was seeing, tied those concerns to specific payroll practices, and escalated them beyond the confines of City Hall. Her actions moved the issue into the hands of Ohio Auditor of State Special Investigations Unit, where cases are opened under statutory authority and not administrative curiosity. The investigation was handled by named state officials, including Cara Yoder and Greg Kopniske, who were tasked with examining whether the conduct surrounding payroll practices could be substantiated through records, interviews, and compelled production of documents.

At the same time, the matter did not remain isolated from the agencies being examined. The Lorain Police Department was not merely adjacent to the investigation. It was embedded within it, both as a subject of review and as a source of records that were requested, questioned, and at times not produced in a manner that satisfied oversight requirements. The involvement of James McCann, whose compensation structure and authority over higher position pay became central to the inquiry, placed the department at the center of the evidentiary record rather than on its periphery. That record also reached into the Lorain County Prosecutor’s Office, where the role of J.D. Tomlinson raised conflict concerns documented within the investigation itself, further complicating the pathway from findings to potential prosecution.

By the time the investigation was fully underway, the issue had expanded beyond a single department or a single transaction. It had become a multi-department examination of how public funds were authorized, how compensation decisions were made, how those decisions were recorded, and whether the documentation supporting them could withstand scrutiny. The question was no longer whether irregularities existed. The question was how those irregularities operated within the system and whether they could be proven in a way that satisfied the legal standard required to bring charges.

That is where this case separates itself from the public narrative that would later define it. The official conclusion is straightforward and has been repeated in exactly that way. There was not sufficient evidence to support criminal charges. That sentence is clean, definitive, and final in the way official outcomes are meant to be. It closes files, ends investigations, and becomes the shorthand explanation for everything that came before it.

But that sentence does not answer the underlying questions raised by the record. It does not state that the conduct did not occur. It does not affirm that the payments were appropriate. It does not confirm that the system functioned as intended. What it states is far narrower. It reflects that the evidence available could not meet the threshold required to prove criminal liability beyond a reasonable doubt.

The documents that led to that conclusion tell a far more complex story. They exist in the form of internal emails, investigative memoranda, interview summaries, payroll records, and repeated requests for documentation that were not consistently fulfilled. Within those documents are statements attributed to officials acknowledging that the governing language for higher position pay was “poorly worded and ripe for abuse.” There are documented instances where records that should have existed were not produced when requested. There are communications from the City Auditor herself noting that the combination of irregular payments and lack of cooperation raised concerns about potential criminal activity.

This is not a case defined by the absence of evidence. It is a case defined by the inability of the system to produce clear, consistent, and verifiable evidence at the moment it was required most. The conduct did not disappear. The documentation did not align. The authority to approve, assign, and pay compensation operated within a structure that diffused responsibility rather than anchoring it.

Once that framework is understood, the outcome ceases to be surprising. A system built on discretionary authority, ambiguous standards, and inconsistent documentation does not collapse because nothing happened. It collapses because too much happened in a way that could not be cleanly reconstructed, and without that reconstruction, accountability becomes increasingly difficult to establish under the law.

II. THE COMPLAINT THAT STARTED IT ALL

Every investigation has an origin point, and in this case that origin is documented, named, and grounded in official responsibility. This did not begin with rumor, speculation, or political dispute. It began with Karen Shawver, the individual legally responsible for overseeing the City of Lorain’s financial records, identifying irregularities within the very payroll systems she was charged with maintaining. That distinction matters because this was not an external allegation imposed on the City. This was an internal alarm raised by the person whose role exists to detect precisely this type of issue.

From the outset, the complaint was structured, specific, and tied directly to verifiable records. It did not rely on broad accusations or generalized concerns. It identified three distinct categories of potential misconduct that extended across multiple departments and functions of city government, each supported by payroll data and internal financial records.

The first category involved excessive overtime within the Utilities and Administrative divisions, where the recorded hours did not align with expected workload demands or historical patterns previously observed within those same departments. The second category focused on irregular payroll practices within the Lorain Police Department, including compensation structures tied to command-level personnel such as James McCann and supervisory staff operating under him. The third category raised concerns within the Law Department, where full-time compensation appeared to be issued in circumstances where the underlying work activity did not clearly reflect full-time hours or consistent documentation of duties performed.

These were not abstract concerns. They were tied to identifiable employees, specific payroll entries, and defined time periods. When Shawver communicated these concerns to the Ohio Auditor of State, she was not asked to clarify vague allegations. She was asked to produce names, dates, departments, and supporting payroll records. That exchange is significant because it demonstrates that the complaint met the threshold required for state-level engagement. The matter was not dismissed. It was accepted, documented, and expanded into a formal investigative process handled by individuals including Cara Yoder and Greg Kopniske.

The scope of the complaint also reveals how quickly the issue moved beyond any single department or isolated transaction. This was not limited to overtime discrepancies. It was not confined to one office or one set of employees. It reflected patterns emerging simultaneously in utilities, law enforcement, and legal administration, all pointing toward a broader breakdown in how payroll was being calculated, authorized, and recorded. What connected these patterns was not the specific job function, but the underlying issue that payroll entries did not consistently correspond to clearly documented, verifiable work activity.

Shawver responded in the manner expected of a financial oversight official operating within statutory obligations. She did not assume intent, and she did not leap to conclusions. She analyzed the data. She compared payroll records against job classifications, departmental structures, and supervisory hierarchies. She examined whether the compensation being issued aligned with the duties that were actually assigned and performed. She requested documentation that should have existed as a matter of routine administrative practice if the system was functioning properly.

What emerged from that process was not a single clerical error or an isolated miscalculation that could be corrected through internal adjustment.

The record reflects repeated instances where payroll entries did not align with organizational structure, where compensation was justified through classifications that did not clearly match assigned roles, and where documentation expected to support those decisions was not readily available when requested.

As the complaint progressed, Shawver’s role necessarily evolved. The process moved beyond routine oversight into investigative inquiry. Her communications became more direct, her requests more specific, and her expectations of compliance more explicit. Each step taken to clarify the records revealed additional inconsistencies, reinforcing the conclusion that the issue was not confined to a single transaction or department. The pattern did not resolve itself as more information was gathered. It expanded. And with that expansion came the realization that the problem was not isolated. It was systemic.

III. THE UTILITIES DEPARTMENT — WHERE THE NUMBERS STOPPED MAKING SENSE

If the complaint established the framework of concern, the Utilities Department is where that framework began to fracture under scrutiny in a way that could no longer be explained as administrative variation or clerical inconsistency. This is the point in the record where the investigation moves from general concern into specific, traceable conduct, where payroll entries are no longer abstract figures but become tied to real employees, real compensation decisions, and a chain of authority that should exist in documented form but instead begins to disappear under examination.

The issue did not emerge in isolation, and it did not remain contained within a single department. By the time Karen Shawver raised these concerns to the Ohio Auditor of State Special Investigations Unit, the investigation had already expanded to include multiple departments, including the Lorain Police Department, and had drawn the attention of state investigators such as Cara Yoder and Greg Kopniske. The seriousness of the concerns is reflected in the fact that subpoenas were issued under statutory authority, compelling production of payroll and timekeeping records, not only from the City itself but from external systems such as Kronos and UKG. Those subpoenas demanded records showing “dates and times actually worked” and “any instances of higher position pay earned,” making clear that the investigation was no longer relying on internal explanations alone but was attempting to independently verify the accuracy of the City’s records.

Within that broader investigative context, the Utilities Department provides one of the clearest examples of how the system functioned in practice.

The internal file repeatedly returns to a specific scenario because it captures the underlying problem in its simplest form. An employee was receiving higher position pay while operating outside the structural conditions that would normally justify that compensation. There was no documented vacancy. There was no formal reassignment. There was no clear supervisory alignment placing that employee into the higher role.

Despite the absence of those required elements, the justification offered was that the duties being performed were “equivalent” to a higher-level position. That single word becomes central to the entire analysis. Equivalent is not defined within a fixed standard. It does not require a formal designation. It does not require a vacancy to exist. It does not require documentation demonstrating that the employee has assumed the full scope of the higher role. Instead, it allows compensation to be elevated based on interpretation. It allows a decision to be made without triggering the structural safeguards that would normally accompany a change in classification, assignment, or authority. Once that interpretation is accepted, the system no longer relies on objective criteria. It relies on discretionary judgment.

The implications of that shift are immediate and far-reaching. Once compensation can be elevated based on undefined equivalency, the need for formal documentation begins to erode. The requirement for a clearly identifiable approval process becomes less rigid. The expectation that payroll entries will correspond to documented assignments weakens. The system continues to function in the sense that payments are processed and recorded, but it loses the ability to demonstrate why those payments were appropriate.

Shawver recognized that problem as it was occurring, not after the fact. The questions she raised were not speculative or theoretical. They were the foundational questions any accountable payroll system must be able to answer. Who authorized the higher position pay. What position was vacant. Where is the documentation supporting the assignment. What record exists to show that the duties performed matched the classification being paid. Those questions are not optional within a functioning system. They are the baseline requirements that allow compensation decisions to be verified.

The responses she received did not resolve those questions. They multiplied them. Supervisors indicated that they had not authorized the change. Other individuals suggested that approval must have come from a higher administrative level. Some responses implied that the arrangement had already been accepted and processed through payroll as part of standard practice. These explanations did not align with one another. They overlapped, contradicted, and shifted depending on who was providing the answer and what portion of the process they were connected to.

This breakdown was not limited to internal explanations. The need to issue subpoenas to external systems such as Kronos and UKG demonstrates that investigators did not consider the City’s internal records sufficient to resolve the issue. When those external systems were contacted, the response further complicated the investigation. The vendor indicated that it did not have access to the relevant TeleStaff data, meaning that the records necessary to verify actual work activity and assignments could only exist within the City’s own systems, the same systems that were already failing to produce consistent documentation.

The investigative record reflects the consequence of that failure. Shawver was unable to identify a single, definitive point of authorization supported by documentation. That absence is not a minor administrative gap. It represents the collapse of the chain of accountability. In a properly functioning system, compensation at a higher level is tied to a documented decision, supported by records, and traceable through a clear line of authority. In this case, that line does not resolve at a single point. It disperses.

What makes this particularly significant is that the payment itself was never prevented. The payroll system processed the compensation. The funds were issued. The transaction became part of the official financial record. The system performed its mechanical function exactly as designed. What it could not do was explain how the decision leading to that payment was made in a way that could be verified after the fact.

That is the moment where an irregularity becomes something more than an administrative issue. It becomes a structural problem. Each layer of the organization acknowledged some portion of the process, but none could anchor the decision within a documented framework that satisfied oversight. Authority existed. Decisions were made. Payments were issued. What did not exist was a record that connected those elements in a way that could withstand scrutiny.

The Utilities Department example does not stand out because of the amount of money involved. It stands out because it exposes the mechanics of how the system operated. It shows how compensation could move through the system based on interpretation rather than documented assignment. It shows how authority could be exercised without producing a consistent record. It shows how a system can continue to function operationally while losing the ability to explain itself.

That is where the numbers stop making sense. Not because they are incorrect in isolation, but because the structure that is supposed to give those numbers meaning no longer exists in a form that can be verified.

IV. THE DOCUMENTATION THAT NEVER SHOWED UP

At a certain point, every investigation reaches a threshold where the focus shifts away from reconstructing events and moves directly into whether those events can be proven through records that should already exist. That transition is visible in this file, and it is not subtle. The questions stop being exploratory and become evidentiary. It is no longer enough for Karen Shawver to identify irregularities in payroll patterns. The system must now demonstrate, through documentation, how those payments were authorized, who approved them, and whether the conditions required for those payments were actually met.

On paper, the City of Lorain had a mechanism designed to do exactly that. Higher Position Pay was not intended to operate on assumption or informal understanding. It required a documented process. Employees were required to complete Higher Position Pay forms identifying the assignment, the duties performed, and the authority under which the assignment was made. Those forms were to be submitted to payroll and retained as part of the official financial record. That process was not theoretical. It was confirmed within the investigative file and recognized by state investigators, including Cara Yoder and Greg Kopniske, as the control mechanism that converted discretionary decisions into something that could be reviewed and verified.

In a functioning system, those forms would be the first and most reliable source of information when questions arise. They would identify the employee receiving the higher compensation, the dates of the assignment, the duties performed, and the individual who authorized the pay. They would create a clear and traceable record connecting decision to payment. They would allow an auditor, a supervisor, or an investigator to reconstruct the transaction without relying on interpretation or memory. That is not what occurred.

When Shawver began requesting those forms, they were not produced. The requests were not vague. They were specific, repeated, and tied directly to identifiable payroll entries. The expectation was clear that the documentation existed because the system required it to exist. The response, however, was consistent in a different way. The documentation was not provided. Requests were followed by additional requests. Follow-ups were made. Deadlines passed. The forms that should have been readily available as part of routine payroll processing were not delivered.

This pattern is reflected throughout the investigative record and becomes more significant when viewed alongside the broader actions taken by the State. Subpoenas were issued under statutory authority, compelling production of records not only from the City but from external systems such as Kronos and UKG. Those subpoenas specifically demanded documentation showing actual work activity and instances of higher position pay. The fact that those subpoenas were necessary demonstrates that investigators did not consider the City’s internal production of records sufficient to answer the questions being raised. When external systems were contacted, the response further underscored the problem. The vendor indicated that it did not possess the relevant TeleStaff data, confirming that the records required to verify assignments and hours worked could only exist within the City’s own systems, the same systems that were failing to produce documentation when requested.

As this pattern continued, the tone of Shawver’s communications changed in a way that reflects the seriousness of the situation. What began as routine oversight evolved into direct and increasingly urgent demands for compliance. The absence of documentation was no longer treated as a delay. It was treated as a failure. In communications to state investigators, Shawver documented that requests for information were being ignored and that the lack of response was occurring while payments tied to Higher Position Pay continued to be processed. That combination is critical. The system was not paused while documentation was located. It continued to issue compensation while the records required to justify that compensation remained unavailable.

The distinction between missing paperwork and a control failure becomes central at this stage. A paperwork issue implies that the records exist but have not yet been delivered. A control failure indicates that the system is not reliably generating, maintaining, or enforcing the documentation required to support its own financial decisions.

The evidence in this record points to the latter. Payments were being authorized and processed without a consistent, verifiable record that could later explain why those payments were made.

The consequences of that failure extend beyond any single transaction. Without documentation, there is no reliable method to confirm whether the conditions for Higher Position Pay were satisfied. There is no way to verify whether an employee was properly assigned to a higher role, whether the duties performed matched the classification being paid, or whether the approval came from the appropriate authority. Each missing form removes a critical link in the chain that connects authority, assignment, and compensation.

What makes this section of the record particularly significant is that the absence of documentation is not isolated. It appears across multiple requests, multiple employees, and multiple departments. It coincides with the need for state-issued subpoenas, with the inability of external systems to provide verification, and with documented statements from the Auditor that her requests for information were not being met. When viewed together, these elements establish that the system, when tested under scrutiny, could not consistently produce the records it was designed to generate.

At that point, the issue is no longer confined to whether specific payments were proper. It becomes a question of whether the system itself is capable of demonstrating that it is functioning correctly. A payroll system that cannot produce its own supporting documentation when challenged is not simply difficult to audit. It is incapable of proving that its outcomes are valid.

That is why this stage of the investigation matters. It marks the transition from identifying irregularities to confronting a deeper structural problem. The system did not just produce questionable results. It failed to preserve the documentation necessary to explain those results when accountability required it. That is not a clerical error. It is the collapse of the controls that are supposed to make accountability possible.

V. WHEN AN AUDIT STARTS SOUNDING LIKE A CRIMINAL INVESTIGATION

There is a point in this record where the language changes, and when the language changes, the nature of the investigation changes with it. What began as a financial review led by Karen Shawver does not remain confined to questions of compliance or administrative correction. It begins to take on the tone, structure, and concern of something far more serious, something that moves beyond whether procedures were followed and into whether the conduct itself may violate the law.

That shift does not occur suddenly. It builds over time as requests for documentation are made, followed, repeated, and ultimately not satisfied in a way that allows the system to explain itself. As Shawver continued to press for records tied to higher position pay, overtime, and departmental compensation practices, her role evolved from reviewing what was available to confronting what was missing. The requests became more direct. The expectations became explicit. The process moved from observation to verification, and the system was no longer simply being reviewed. It was being tested under conditions that required it to produce answers.

At the same time, the investigation had already expanded beyond the City’s internal processes. The involvement of Cara Yoder and Greg Kopniske placed the matter within the authority of the Ohio Auditor of State Special Investigations Unit, where subpoenas were issued under statutory authority to compel production of payroll and timekeeping records. Those subpoenas reached not only into City departments such as the Lorain Police Department, where individuals including James McCann and command staff were identified within the scope of the inquiry, but also extended outward to third-party systems such as Kronos and UKG in an effort to independently verify work activity and compensation.

Despite that escalation, the system did not respond with the clarity that would be expected in a functioning structure. Documentation continued to go unproduced. External systems could not provide the necessary data. Internal records did not align in a way that allowed investigators to reconstruct decisions with confidence. The breakdown was no longer limited to isolated discrepancies. It had become a pattern.

That pattern is captured in one of the most significant moments in the investigative record. Shawver put into writing that the combination of irregular payments and the lack of cooperation she was encountering raised concerns that criminal activity could be occurring within the Utilities Department.

This is not speculative language. It is a formal statement made by the City’s financial oversight authority, directed to state investigators already operating under fraud investigation authority. It reflects a conclusion formed after repeated attempts to obtain documentation, after identifying compensation patterns that did not align with standard practices, and after encountering resistance in circumstances where transparency should have been immediate.

The significance of that statement lies not only in what it says, but in what it represents. Once an Auditor identifies the possibility of criminal conduct, the investigation crosses a threshold. It is no longer limited to correcting procedures or addressing administrative deficiencies. It carries the potential for referral, for prosecution, and for individual accountability under statutes governing misuse of public funds, falsification of records, and unauthorized compensation. The presence of state investigators, the issuance of subpoenas, and the documented concerns of the Auditor collectively establish that this threshold was reached. And yet, this is also the point where the investigation begins to slow.

The concerns do not diminish. The irregularities do not resolve. The requests for documentation do not become less urgent. What changes is the ability of the system to produce the type of evidence required to move forward. The same conditions that allowed the irregularities to occur begin to obstruct the ability to prove them. Documentation that should establish authorization is missing. Records that should verify work activity are unreliable or unavailable. External systems cannot supply independent confirmation. The chain of approval cannot be reconstructed in a way that ties decision to action with certainty. Authority is distributed across multiple individuals and departments, diffusing responsibility rather than concentrating it.

The investigation does not lose momentum because the issue disappears. It loses momentum because the evidentiary foundation required to sustain criminal charges cannot be built from what is available. That is the central paradox of this case. Shawver identifies patterns that raise legitimate concern. The lack of cooperation reinforces those concerns. The absence of documentation deepens them. The involvement of state investigators confirms that the matter has reached a level of seriousness that warrants formal inquiry.

And still, the system cannot produce proof that meets the legal standard required to charge anyone.

That outcome is not the same as exoneration. It does not establish that the conduct was proper. It does not confirm that the payments were justified. It reflects the limitation of the evidence within the structure of the system. The investigation, at this stage, begins to resemble a criminal case in every way except one. It raises the same questions, identifies the same potential violations, and confronts the same patterns that would exist in a prosecutable matter. What it lacks is not suspicion. What it lacks is provability. And that distinction becomes the defining feature of everything that follows.

VI. THE POLICE SIDE — WHERE THE SYSTEM EXPLAINS ITSELF

If the Utilities Department shows how the system could be used, the Police Department explains why the same system could not be definitively challenged. This is the point in the record where the investigation moves beyond identifying irregularities and begins confronting a deeper structural problem, one rooted not in isolated decisions but in how authority, documentation, and compensation were configured within the Lorain Police Department itself.

The individuals at the center of this portion of the investigation were not rank-and-file employees operating at the margins of the system. They were command-level officials whose roles directly intersected with how higher position pay was assigned and processed, including James McCann, Michael Failing, A.J. Mathewson, Corey Middlebrooks, and Les Palmer. These were the positions where decisions regarding availability, assignment, and compensation were made, approved, and translated into payroll.

What the investigation uncovered within that structure was not simply inconsistency. It was the absence of a reliable mechanism to verify the very conditions that triggered higher compensation.

The findings tied to the Chief’s role are central to understanding that breakdown. As a salaried, overtime-exempt employee, McCann’s time was not tracked in a way that could be used for verification. The department relied on the TeleStaff system, but that system did not function as a record of actual hours worked. It operated as a default entry system, recording a standard forty-hour workweek regardless of the Chief’s actual activity.

The Auditor stated it directly in the record. “TeleStaff does not reflect the Chief’s actual time worked… the Chief has a default of 40 hours per week… TeleStaff cannot be used as a source to determine hours of work performed.”

That statement removes the foundation that would normally allow compensation decisions to be tested against objective data. If the system cannot confirm when the Chief was working, it cannot confirm when the Chief was not working. Without that distinction, the conditions used to justify higher position pay cannot be anchored to a verifiable record.

That structural gap is compounded by how higher position pay was triggered within the department. Compensation at the captain level, including for individuals such as Failing and Mathewson, was not tied to a documented absence supported by time records. It was tied to whether the Chief was considered “unavailable.” That distinction replaces an objective condition with a subjective determination.

The record identifies where that determination was made. “The Chief (or his designee) has sole authority to determine if HPP is required and who is assigned.”

That authority consolidates both sides of the compensation decision within the same control point. The Chief determines his own availability, and that determination directly results in higher position pay being assigned to other members of the command staff. The system does not require an independent verification of that status, nor does it produce a record that allows that determination to be tested after the fact.

The implications of that structure are reflected in the payroll patterns that prompted the investigation. The Auditor identified instances where compensation appeared to overlap in a way that could not be reconciled through available records. Multiple individuals appeared to be receiving compensation tied to the Chief’s role during the same period.

The concern was articulated clearly within the investigative file. “It is not… lawful, that two people are being paid the chief’s wages at the same time.”

In a system grounded in clear documentation, that question could be answered through records showing when the Chief was absent, when another individual was formally assigned to act in that capacity, and whether the compensation aligned with those assignments. The record would provide a definitive account of how and why the payments were made.

In this system, those answers could not be produced with certainty. The Chief could be considered unavailable while still performing work. The Chief could be designated as unavailable without a corresponding record of absence. The system did not preserve a distinction between those conditions in a way that allowed for independent verification.

This is the point where the investigation encounters its structural limit. The issue is not whether the payments can be questioned or whether overlapping compensation can be identified. Both can be done. The issue is that the system does not provide a reliable method to determine whether those payments were proper or improper under the rules that governed them.

Without an objective standard tied to documented work activity, there is no fixed point against which the conduct can be measured. The analysis becomes dependent on interpretation rather than verification. What one individual may view as justified compensation based on availability, another may view as overlapping or excessive pay. The system itself does not resolve that distinction because it was not designed to.

That is why this portion of the investigation is so significant. It does not simply show how higher position pay was applied within the department. It shows why the system resisted being pinned down when those applications were challenged. Authority was concentrated, documentation was limited, and the standards required to verify decisions were undefined in practice. The system continued to produce outcomes. What it could not produce was clarity. And without clarity, accountability becomes increasingly difficult to establish.

VII. THE DATA THAT UNDERCUT THE DEFENSE

At a certain point in the investigation, the argument that everything was operating normally stopped being sustainable, not because of speculation or interpretation, but because of what the numbers themselves revealed when placed side by side over time. In cases involving payroll and public funds, the most predictable defense is not that nothing happened, but that whatever did happen was routine, expected, and consistent with how the system has always functioned. That argument only survives if the underlying data reflects a stable and repeatable pattern. When the data begins to show divergence within the same role, under the same structure, the foundation of that defense begins to collapse under its own weight.

This is precisely the method employed by Karen Shawver as she continued to work alongside the investigative team from the Ohio Auditor of State Special Investigations Unit, including Cara Yoder and Greg Kopniske. The approach was not complex, but it was precise. Instead of comparing different departments or unrelated classifications, the analysis focused on the same position across different employees performing the same function at different points in time. By removing as many external variables as possible, the comparison isolated the role itself and allowed the investigation to focus on how that role was actually compensated.

The analysis relied on payroll records, overtime entries, and the presence or absence of higher position pay tied directly to that position. It did not depend on interpretation or narrative. It depended on recorded financial data that could be examined independently of explanation.

What that comparison revealed was not consistency, but a clear and measurable departure from prior practice. A previous employee occupying the role performed the same core responsibilities with compensation that remained within expected parameters. Overtime was limited, and there was no reliance on higher position pay to supplement the base salary. The position functioned within a structure that aligned with both the organizational hierarchy and the documented expectations of the role.

When that same position was later filled by another employee, the compensation profile changed in a way that could not be attributed to the position itself. Overtime increased in both frequency and volume. Higher position pay was introduced and layered onto the base compensation. The financial footprint associated with the role expanded significantly, despite the absence of any documented reclassification of duties, formal reassignment, or structural change that would justify that increase.

That divergence is critical because it removes the most accessible defense available to the system. If the compensation patterns observed during the investigation were inherent to the role, they would appear consistently regardless of who occupied the position. The absence of those patterns in the earlier period, followed by their emergence in the later period, demonstrates that the change was not driven by the demands of the job itself. It was driven by how the job was being managed, interpreted, and compensated within the system.

This is the same system that, by this stage of the investigation, had already been shown to lack reliable documentation, to rely on discretionary determinations for higher position pay, and to require subpoenas to attempt to reconstruct basic payroll activity. When that system produces materially different compensation outcomes for the same role, the explanation cannot be found in the position. It must be found in the decisions that surrounded it.

The comparison forces a question that cannot be avoided once the data is placed in context. If the role did not historically require elevated overtime or layered compensation, what changed to justify those payments later. The answer cannot be found in the duties, because the duties remained materially consistent. The answer must be found in how overtime was authorized, how higher position pay was applied, and how those decisions were processed through a system that has already been shown to lack consistent documentation and objective verification.

What makes this portion of the investigation particularly significant is that it does not rely on inference, assumption, or conflicting testimony. It relies on direct comparison of recorded data across time. It demonstrates that the system did not operate in a uniform manner and that the compensation patterns under review were not consistent with prior execution of the same role. That finding does not resolve every question raised by the investigation, but it eliminates one of the most common explanations used to defend questionable payroll practices.

Once that explanation is removed, the discussion necessarily shifts. The issue is no longer whether the system allowed the conduct to occur, because the data shows that it did. The issue becomes whether that conduct can be justified within the framework the system was supposed to enforce, and whether the absence of consistency, documentation, and verification can be reconciled with the obligation to account for the use of public funds.

VIII. THE SYSTEM WAS NOT HIDDEN — IT WAS BUILT THIS WAY

By the time the investigation reached its conclusion, the most uncomfortable reality was no longer avoidable, and it was not rooted in a hidden scheme or a single point of failure that could be isolated and corrected. The issue was structural. The system, as it existed within the City of Lorain, allowed the very conduct that triggered the investigation. It did not require concealment because it operated within the boundaries of how authority was defined, how compensation was interpreted, and how records were maintained across departments including the Lorain Police Department and the Utilities division.

What emerges from the record is not a system that collapsed under pressure, but one that functioned exactly as it was designed to function when tested.

The framework governing higher position pay did not require rigid triggers tied to clearly documented vacancies or formal reassignment. Instead, it allowed compensation to be elevated based on the concept of “equivalent duties,” language that was acknowledged within the investigation itself as lacking a fixed definition and being “poorly worded and ripe for abuse.” That phrase is not commentary. It is an admission embedded within the record, tied to discussions involving officials such as Patrick Riley and others responsible for interpreting the contractual and policy language that governed compensation.

Once that standard was accepted, the system no longer required objective proof to support elevated pay. It required interpretation. It allowed decisions to be made without the structural safeguards that would normally anchor those decisions to documented changes in assignment, authority, or responsibility. The requirement for a vacancy could be bypassed. The requirement for a formal appointment could be bypassed. The requirement for a clearly defined shift in duties could be replaced with a determination that the work being performed was sufficiently similar to justify higher compensation.

At the same time, the system lacked a uniform method for tracking time at the level where those determinations were most consequential. As established in the investigation involving James McCann and command staff including Michael Failing and A.J. Mathewson, the TeleStaff system did not function as a reliable record of actual hours worked. It defaulted to a standard forty-hour entry regardless of reality, and it could not be used to determine when the Chief was present, absent, or available in a way that could be verified. Without that data, the system lost the ability to establish the very condition that triggered higher position pay.

Authorization within this structure flowed through multiple layers of authority, but those layers did not consistently produce documentation that could be traced after the fact. Decisions were made by individuals within the command structure, including the Chief and those operating under his authority, and those decisions were processed through payroll. The outcome of those decisions was recorded in the form of compensation. What was not consistently preserved was the reasoning behind those decisions in a way that allowed them to be reviewed, challenged, or verified under scrutiny.

This lack of traceability is not incidental. It is structural. It creates a system where outcomes exist in the financial record, but the path that led to those outcomes cannot be reconstructed with certainty.

When Karen Shawver requested documentation to support those decisions, the response was not the production of a complete and consistent record. Requests went unanswered or were delayed. Forms that should have existed were not produced. Subpoenas had to be issued by the State through Cara Yoder and Greg Kopniske in an attempt to obtain records that should have been available through routine administrative processes.

Even then, the system did not produce clarity. External vendors such as UKG confirmed that they did not possess the data necessary to verify TeleStaff activity, reinforcing that the only place those records could exist was within the City itself, where documentation had already been shown to be inconsistent or unavailable. The payroll system continued to function mechanically, processing the information it was given without independently verifying whether that information met the conditions required by policy. If a higher position assignment was entered, the system calculated the pay. If overtime was submitted, the system applied it. The process depended entirely on the integrity of the inputs rather than testing them against an independent standard.

When Shawver attempted to enforce the controls that were supposed to exist within this framework, those controls did not hold. The expectation that documentation would be produced was not met. The expectation that assignments would be traceable was not satisfied. The expectation that compensation decisions could be verified against objective records proved unfounded. The mechanisms designed to ensure accountability did not fail in a moment of crisis. They failed when they were asked to operate as intended.

All of these elements converge into a single conclusion that cannot be avoided once the record is read in full. The system did not conceal the conduct. It allowed it. It provided a structure in which compensation decisions could be made based on interpretation, processed without consistent verification, and recorded without preserving a clear chain of authority.

That structure blurred the distinction between what was permitted and what might constitute misuse. It did so not through isolated error, but through the way the rules were written, interpreted, and enforced across departments and individuals. The same features that allowed compensation to be elevated also prevented those decisions from being cleanly evaluated under a legal standard that requires clear, documented proof.

This is why the investigation ultimately reached a limit that could not be overcome. The absence of clear standards, the lack of consistent documentation, and the reliance on subjective determinations created an environment where irregularities could exist without producing the kind of definitive evidence required for prosecution.

The outcome does not resolve whether the conduct was appropriate. It reflects whether the system was capable of proving that it was not.

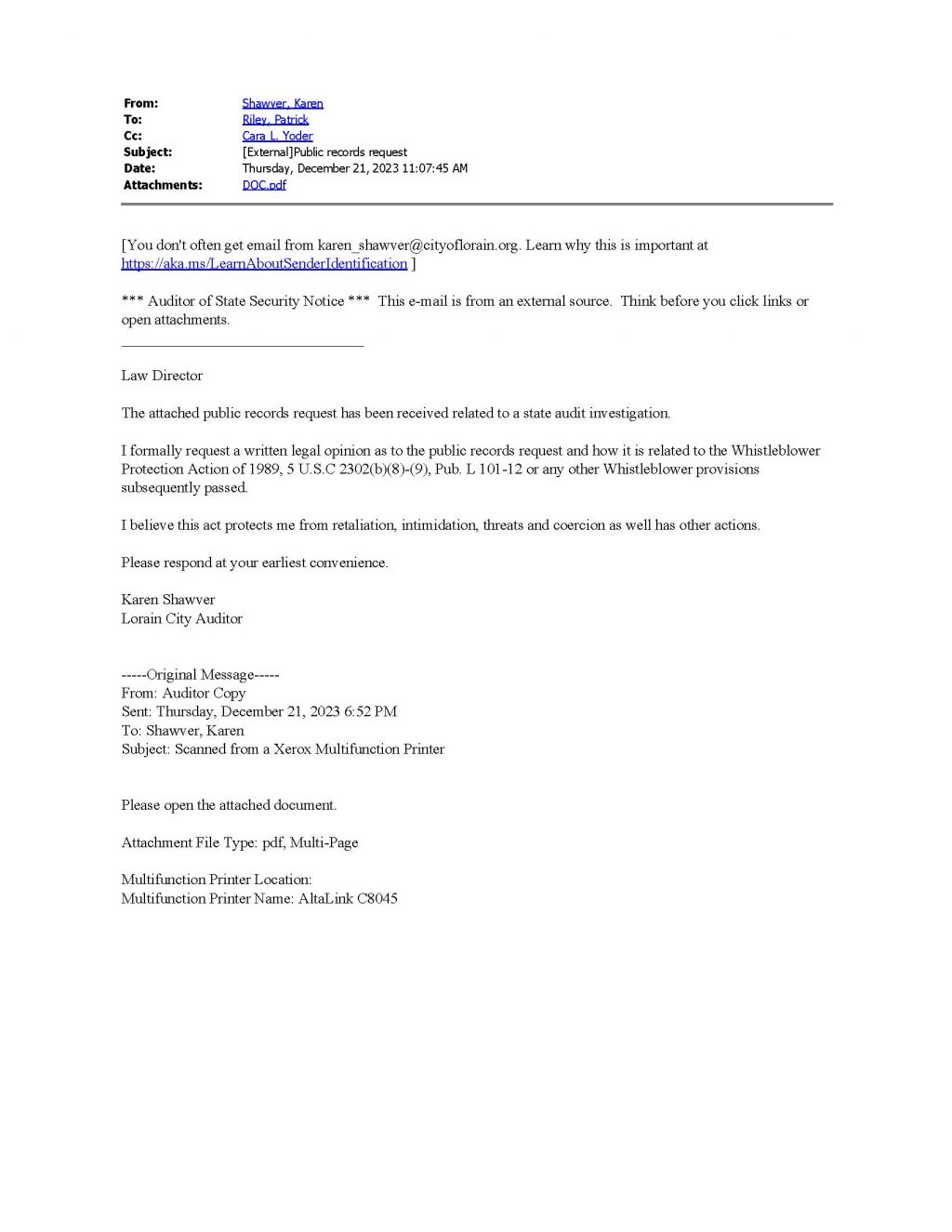

IX. THE WHISTLEBLOWER MOMENT

The final layer in the record is not financial, procedural, or structural. It is personal, and that is what makes it so revealing. After months of tracing payroll, requesting documentation, and confronting inconsistencies across departments including the Lorain Police Department, the role of Karen Shawver begins to change in a way that is visible in her own words. The focus is no longer limited to reconciling numbers or enforcing compliance within a routine audit framework. It expands to include her own position within the process and the risks associated with continuing to push forward against resistance that had become persistent and, at times, unresponsive.

That shift is not inferred. It is documented. In communications with state investigators, including Cara Yoder and Greg Kopniske, Shawver begins asking questions that do not appear in standard financial oversight. She seeks guidance on legal protections available to her. She raises concerns about how her continued efforts to obtain documentation and enforce accountability may be received within the administration.

She [Shawver] explicitly references the need for protection against retaliation, intimidation, and coercion, framing her actions within the context of whistleblower safeguards rather than routine administrative duty.

That is a significant development because it signals a change in the environment surrounding the investigation. An auditor operating within a functional system does not typically need to consider whistleblower protections in order to perform basic oversight responsibilities. Those protections become relevant when the act of asking for records and enforcing compliance is no longer neutral, when resistance replaces cooperation, and when the possibility of personal or professional consequence becomes part of the equation.

The record reflects that this was not a hypothetical concern. As Shawver continued to request documentation tied to higher position pay, overtime, and compensation practices involving individuals such as James McCann and command staff including Michael Failing and A.J. Mathewson, the responses she received did not resolve the underlying questions. Instead, she was directed to route legal questions through Patrick Riley. When those avenues did not produce clear answers, she was advised that the matter could be elevated to City Council or addressed through outside counsel.

That sequence of events reflects more than administrative procedure. It reflects a breakdown in the normal flow of information that should exist within a system responsible for managing public funds. Instead of receiving direct answers from the departments involved, the Auditor was navigating layers of authority in an effort to obtain basic clarity about how compensation decisions were being made and documented. The process shifted from resolving discrepancies to managing access to information.

What emerges from this portion of the record is a clear indication that the investigation had moved beyond routine oversight and into an adversarial posture. That adversarial nature is not defined by formal litigation, but by the practical reality that requests for information were met with delay, redirection, or non-response. The system was no longer operating in a way that allowed the Auditor to verify its outputs through standard processes. It was operating in a way that required escalation, persistence, and, ultimately, consideration of personal protection in order to continue.

The decision to invoke or even consider whistleblower protections underscores the extent of that shift. It reflects an understanding that continuing to press for answers could carry consequences beyond the scope of financial oversight. It also reinforces the broader pattern that runs through the entire record. The system did not simply fail to produce documentation when asked. It resisted examination in a way that made it increasingly difficult to establish clear and verifiable conclusions.

This moment does not stand apart from the rest of the investigation. It is the culmination of it. It shows what happens when structural ambiguity, missing documentation, distributed authority, and external investigative pressure converge with an internal oversight process attempting to impose clarity. The result is not resolution in the traditional sense. The result is tension between the obligation to account for public funds and the system’s inability or unwillingness to fully explain itself. That tension becomes the defining characteristic of this stage of the case.

X. NO CHARGES DOES NOT MEAN NO FINDINGS

The official outcome of this investigation will always be reduced to a single line because that is how outcomes are communicated to the public, to the media, and often to the courts. There were no criminal charges. That statement is clean, definitive, and easy to repeat. It closes the file in a way that suggests resolution, but it does not reflect the full weight of what the record actually contains or the extent of what was documented by those directly involved in the investigation.

The absence of charges is not a finding that the system operated properly. It is not a declaration that the payments were appropriate, justified, or supported by complete and reliable documentation. It is a statement about the limits of proof within the framework of criminal law, a framework that requires evidence capable of establishing intent, authorization, and conduct beyond a reasonable doubt. What it reflects is what could not be proven to that standard, not what was observed, recorded, and repeatedly questioned by Karen Shawver and the investigative team from the Ohio Auditor of State Special Investigations Unit, including Cara Yoder and Greg Kopniske.

When the underlying documents are examined in full, the record presents a consistent and layered pattern that spans departments, positions, and decision-making authority. Within the Lorain Police Department, individuals including James McCann, Michael Failing, and A.J. Mathewson were operating within a system where higher position pay could be triggered without a verifiable record of absence or assignment. Within other departments, including Utilities and the Law Department, compensation patterns raised similar concerns about how payroll decisions were being made and documented.

Across all of these areas, the same issues appeared repeatedly. Payroll practices were not uniform. Compensation decisions did not consistently align with clearly documented work activity. Records that should have existed to support those decisions were not always available when requested.

The chain of authorization, which should have been defined, documented, and traceable, could not be consistently reconstructed. Supervisors, administrators, and departments provided explanations that did not align with one another. Responsibility shifted depending on who was asked and what part of the process they were connected to. The absence of a clear, documented approval chain meant that decisions resulting in compensation could not be anchored to a single accountable source. At the same time, the system continued to function operationally. Payments were processed. Payroll entries were recorded. Compensation was issued even as documentation supporting those payments was being requested and not produced.

The tone of the investigation itself reflects the seriousness of these conditions. Shawver did not describe the issues in neutral or procedural terms. She documented that the combination of irregular payments and lack of cooperation raised the possibility of criminal activity.

That statement was made in communication with state investigators operating under fraud investigation authority, and it underscores the level of concern present within the investigative process. It confirms that the issue had moved beyond administrative discrepancy and into potential legal exposure.

What ultimately defines the outcome is not the absence of issues within the system, but the inability of that system to produce clear, consistent, and verifiable answers at the moment they were required. The same structural deficiencies that allowed the compensation patterns to occur also prevented those patterns from being evaluated under a criminal standard. Documentation was incomplete or missing. Time records were unreliable or unavailable. External systems could not provide verification. The chain of authorization could not be definitively established. Without those elements, the evidentiary foundation required to support prosecution could not be built.

This is the distinction that must be understood in order to interpret the outcome accurately. The lack of criminal charges does not mean that the investigation found nothing. It means that the findings existed within a system that could not translate those findings into proof sufficient to meet the legal threshold required for prosecution.

XII. FINAL CLOSING — THIS DID NOT START YESTERDAY, AND IT DID NOT HAPPEN IN A VACUUM

What makes this record impossible to dismiss is that it does not stand alone. This did not begin with payroll. It did not begin with a travel voucher. It did not begin with higher position pay. It sits inside a much longer pattern involving Chief James McCann, the Lorain Police Department, the Law Department, and repeated conflict with me as a citizen, journalist, records requester, and critic who kept asking questions, kept requesting records, and kept documenting what the City did not want exposed.

That long arc matters because patterns matter. In August 2021, when I raised concerns about a civil rights issue involving access and my service animal, McCann wrote, “I take all complaints seriously, but understand, I cannot be involved in every aspect of this department or I wouldn’t need a command staff.” That statement matters because it established the framework McCann wanted everyone to accept. He was the Chief. He delegated. He relied on command staff. He could not be everywhere. But as time went on, when later controversies arose, when records were sought, when complaints multiplied, and when public criticism intensified, the response did not look like distance. It looked like direct control.

By March 2023, the conflict had plainly deepened. In an email responding to criticism about the department’s handling of social media comments and the West 27th Street controversy, McCann wrote that he was “well-aware that a government agency operating a government social media page is subjugated to legal and constitutional constraints” and declared, “To be clear, I am willing and ready to stand in front a Federal Judge to state my case.” He also made it personal, writing, “You claim to be an educated social worker, but one would think with your claim of being educated, you would have the ability and the ‘want’ to get all the facts before you make assumptions.” That was not a neutral administrative response. That was defensive, hostile, and personal, and it came in the middle of a dispute over constitutional rights and public accountability.

Then the control got even more direct. On June 21, 2023, after I asked him to stop emailing me and to communicate by mail, McCann refused. His answer was explicit. “Email is my chosen form of communication to reply to you and all the public information requests I receive from everyone so this is what you get.” He then wrote, “I will be the only one to respond to all your request from now on,” and added, “you don’t get to demand who to talk to at Lorain PD, I get to make those decisions.” Put that next to his earlier claim that he could not be involved in every aspect of the department because he had command staff. The contradiction is glaring. When I was just another citizen with a complaint, he said he could not do everything. When I became a persistent critic and records requester, suddenly everything had to run through him.

That same summer, the conflict spread into other institutions. McCann filed a complaint against my social work license. He later sent a large volume of material about me to Juvenile Court Administrator Tim Wietzel, including information that I maintain was sensitive, retaliatory, and improperly shared. The dispute did not stay inside police records requests. It spread into professional licensure, contract work, juvenile court access, and communications with third parties. It cost me work. It cost me income. And it is exactly why this payroll investigation cannot be treated like some detached, technical financial review. It unfolded in the middle of a long-running pattern of hostility and retaliation.

That context matters because when the payroll issues surfaced, the names in the record were not strangers to later events. Michael Failing appears in the payroll and higher position pay questions. A.J. Mathewson appears in department communications, records responses, and the broader pattern of contact. Patrick Riley appears in the investigative interviews, in the legal interpretation of the compensation structure, and now acts as legal counsel around the very power structure coming after me. That overlap is not some side issue. It is one of the ugliest parts of the whole story. The same network of officials and departments that show up in a state-level payroll investigation are also central figures in the civil and criminal pressure now being applied to the journalist who pursued these records.

That is why the phrase “no charges” does not carry the weight they want it to carry. The issue is not merely that the investigation ended without prosecution. The issue is that a record containing missing documentation, contradictory explanations, subpoenaed records, admitted ambiguity, and direct concern from the City Auditor about possible criminal activity did not produce meaningful transparency. The public was not given a full accounting. Taxpayers were not told exactly how public money moved, who authorized it, why the system could not explain itself, or why nobody appears to have been held financially responsible when the same record describes a structure vulnerable to abuse. And then there is what happened after.

When I turned over my material and the broader pattern to Sheriff Jack Hall’s investigator, what came back was essentially a stripped-down conclusion that there was no crime to see here. Move along. That kind of answer would be bad enough in any case. In this one, it is something worse. It came after the State had already been involved. It came after Karen Shawver had raised concerns in writing. It came after subpoenas. It came after the City’s own failures to produce records cleanly. It came after a developed evidentiary record already existed. To answer all of that with a bare conclusion and no meaningful public explanation is not transparency. It is institutional closure without institutional accountability. And that still is not the end of it.

The same City whose departments and officials were implicated in these records disputes is now prosecuting me on six misdemeanor charges that are, in my view, complete complete fabrications at Bullshit.

I was hit with a seventeen-thousand-dollar bond. I sat in jail for roughly twenty-four hours. They released footage of my arrest and the ride in the police car. The local paper reported on that one incident over and over again. The municipal court is recused, and every court in Lorain either is recused or should be because the conflicts are obvious. That is not a criminal case happening in a vacuum. That is the next chapter in a documented pattern of escalation against the person who kept digging.

The contrast could not be more obvious. When public officials and departments are confronted with records showing structural irregularities in payroll, missing documentation, overlapping compensation, and a system described by its own actors as vulnerable to abuse, the result is no real public accounting, no meaningful transparency, and no visible repayment to the taxpayers who financed it all. When the journalist who pursued those records keeps pressing, the result is prosecution, jail, public spectacle, and relentless local media exposure.

So what is more likely. That I am some violent, uniquely dangerous person who suddenly required extraordinary legal attention, a huge bond, public release of footage, and six separate charges. Or that the City, the Police Department, the Law Department, the Sheriff’s Office, and the local power structure do not like the stories I am telling and have responded exactly the way compromised institutions respond when someone gets too close to the truth.

That is not a rhetorical question. It is rooted in names, dates, emails, subpoenas, payroll records, and the conduct of the very people now trying to drag me through the courts. It is rooted in McCann’s own words. It is rooted in the involvement of Failing, Mathewson, Riley, Wietzel, and others. It is rooted in Shawver’s warnings, in the State’s subpoenas, in the missing records, and in the complete failure of every institution involved to give the public a straightforward explanation of what happened to their money.

The taxpayers of Lorain did not fund opacity. They did not fund a compensation system that cannot explain itself. They did not fund a network of public offices so insulated from scrutiny that even documented concern from the City Auditor and a state investigation can be absorbed without visible consequence. And they certainly did not consent to a system in which the people asking the questions become the ones dragged into court while the people in power stay protected by ambiguity, procedure, and silence.

That is why this story is not over. The payroll record is one part of it. My long-running issues with McCann are another. The retaliatory feel of the later prosecutions, the bond, the footage release, the media saturation, and the conflict-ridden court environment are all part of the same larger question about whether public power in Lorain is being used to inform the public or control it. There is much more to come, and there should be, because this record does not read like closure. It reads like the middle of a much bigger story. Stay tuned.

LEGAL DISCLAIMER

This article is based on public records, investigative materials, and documented communications obtained through lawful means. All statements are presented for informational and journalistic purposes. Any conclusions drawn are based on the totality of the documented record and are not assertions of criminal guilt. All individuals are presumed innocent unless proven otherwise in a court of law.

See all documents here: https://aaronknappunplugged.com/the-lorain-police-and-utilities-timecard-fraud-investigation-files/

Legal Disclaimer

This publication is an investigative commentary based on public records, official documents, and communications obtained through lawful requests, including those made pursuant to Ohio law. The analysis presented reflects the author’s interpretation of those materials and is offered as opinion and reporting on matters of public concern.

Any references to individuals, agencies, or conduct are drawn from documented sources and are presented for the purpose of informing the public. Nothing contained in this article should be interpreted as a formal allegation of criminal guilt. All individuals are presumed innocent unless proven otherwise in a court of law.

This article addresses issues involving government operations, public funds, and official conduct. As such, it constitutes protected speech under the First Amendment, including freedom of the press and the right to comment on matters of public interest.

This content is not legal advice and should not be relied upon as such.

© Unplugged with Knapp Media LLC. All rights reserved.