Stay Titan Strong, but Show the Math

A line by line reality check of Lorain City Schools’ $18 million claim, and the public records that must exist

Byline

By Aaron Knapp

Investigative Journalist

Lorain Politics Unplugged

Introduction

Trust is not a financial control, and reassurance is not documentation

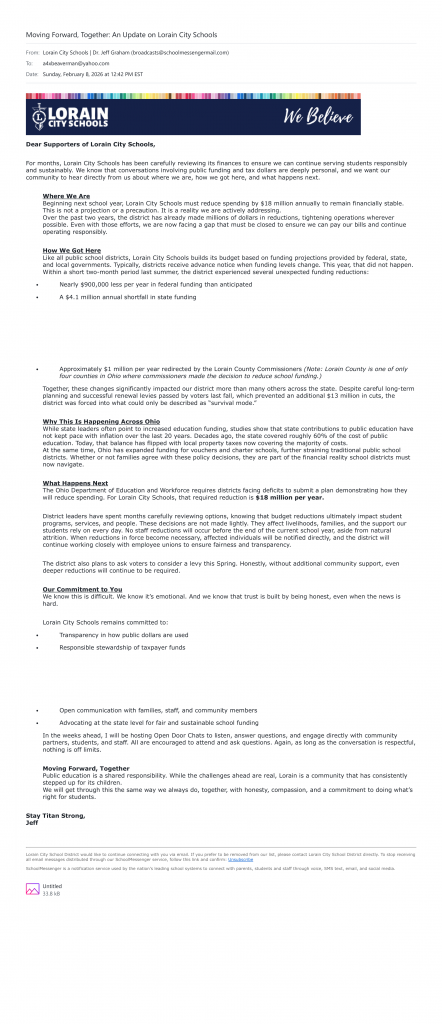

Lorain City Schools has issued a carefully calibrated message to families, staff, and the broader community that asks for confidence before it provides proof. The letter presents an eighteen million dollar annual reduction as unavoidable and imminent. It frames the crisis as the product of sudden, largely external funding hits. It promises no immediate layoffs, signals a levy without terms, and announces listening sessions designed to help the community process what is being described as an already settled outcome.

In doing so, the district makes a series of factual claims that fall into only two categories. They are either verifiable right now through public records, or they are not. That distinction matters because public education is not only personal. It is also public finance, governed by statute, audited through formal forecasts, and justified through records that are not optional.

When a school district tells families that it must cut eighteen million dollars every year, that figure is not an emotion and it is not a narrative device. It is a conclusion.

Conclusions of that magnitude do not appear fully formed. They are produced through five year forecasts, enrollment assumptions, revenue calculations, expenditure baselines, cash flow projections, and written notices from state and federal agencies. They exist because the law requires them to exist.

Over the last two decades, Lorain City Schools has repeatedly asked the public to accept urgency without full transparency. State intervention under House Bill 70 stripped local control while failing to deliver durable academic or financial recovery. Governance authority shifted upward, but accountability never followed cleanly. Decision making became centralized, outcomes stagnated, and a pattern emerged in which conclusions were announced without the underlying analysis being disclosed in real time.

That history matters now, because it informs how the current message should be read. When leadership asserts that the numbers are settled and the path is determined, it is asking the community to trust the same systems that have repeatedly failed to stabilize enrollment, finances, or outcomes.

Public trust is not built by tone. It is built by access.

Ohio law does not require families, employees, or taxpayers to take financial claims on faith, and it does not permit public institutions to substitute reassurance for disclosure. A claim that eighteen million dollars in annual cuts is unavoidable must be supported by documents that already exist if the claim is true.

A current five year forecast showing the deficit trajectory. Assumptions worksheets detailing enrollment, staffing, benefits, transportation, and special education costs. Written notices documenting federal and state funding reductions. Communications with the Ohio Department of Education and Workforce regarding fiscal status or corrective action. Records showing when these numbers were calculated and how they were validated.

This article is not an attack on teachers, support staff, or students, who consistently absorb the consequences of financial decisions they did not make. It is not a denial that school funding is complex or that districts operate under real constraints. It is a demand for informed consent.

Levies, closures, consolidations, and reductions in force are not motivational exercises or appeals to resilience. They are legal and financial decisions that must be justified through forecasts, revenue projections, staffing models, and formal intergovernmental communications. They rise or fall on whether the math supports the narrative.

When leadership asks the public to stay strong, the public is entitled to ask a simpler and more fundamental question. Show the math.

What the District Said, and What It Did Not Say

Confidence without citation is not transparency

The superintendent’s message on behalf of Lorain City Schools is written in a register designed to convey finality. The language is not exploratory and it is not conditional. It does not present a range of outcomes or competing scenarios. It states plainly that the district must reduce spending by eighteen million dollars annually beginning next school year. It emphasizes that this figure is not a projection, not a contingency, and not a precaution. It asserts that millions have already been cut and that the remaining gap must be closed simply to pay bills. Taken together, the message communicates that the analysis is complete and that the only remaining discussion concerns how the community will absorb the consequences, not whether the conclusion itself is sound. That posture matters because language of finality carries an implied claim.

When district leadership speaks as though uncertainty has been resolved, it is implicitly asserting that the underlying documentation exists, has been reviewed, and supports the conclusion beyond reasonable dispute.

In public finance, that level of certainty is not rhetorical. It is documentary.

It is only credible when it is anchored to identifiable records that can be examined by the public. What the message does not provide is the minimal set of references that would allow a taxpayer, employee, or parent to independently verify any of its central assertions. There is no link to the most recent five year forecast, even though that document is the statutory backbone of school district financial planning in Ohio. There is no date identifying which forecast is being relied upon, despite the fact that forecasts are updated on a schedule and assumptions can change materially from one filing to the next. There is no identification of which fund or combination of funds is driving the claimed deficit, a critical omission given that districts operate multiple funds with different balances, restrictions, and legal uses.

The letter also omits any explanation of causation at the expenditure level. It does not explain which costs became structurally recurring and why, nor does it distinguish those from temporary or discretionary expenditures that could be reduced or reversed without permanent harm. It does not explain which revenues declined, when those declines occurred, or whether those revenues were ever appropriate to treat as ongoing in the first place. Absent that information, the eighteen million dollar figure appears as an outcome without a pathway, a conclusion presented without the chain of decisions and assumptions that produced it. Most notably, the message provides no functional breakdown of the reduction itself. There is no disclosure of what portion of the eighteen million dollars is attributed to staffing versus non personnel costs. There is no indication of how much relates to transportation, special education obligations, facilities, debt service, or administrative overhead.

Those categories are not academic abstractions. They are the difference between classroom impact and back office adjustment. They are the difference between compliance driven costs imposed by law and policy driven choices made by leadership. Without that breakdown, the public is left to infer consequences without understanding their source.

A community cannot evaluate necessity without those details.

It cannot assess whether cuts are truly unavoidable or whether they reflect a particular set of priorities embedded in the forecast assumptions. It cannot judge whether leadership exhausted alternatives before turning to reductions and levies. And it cannot meaningfully participate in listening sessions that solicit feedback on outcomes while withholding the analysis that produced them.Transparency does not require agreement with the district’s conclusions, but it does require that the public be given access to the same information leadership claims to be using when it declares the path already determined.

The Eighteen Million Dollar Figure Should Be Traceable in the District’s Five Year Forecast

Where the law requires the math to live

Under Ohio law, Lorain City Schools is required to prepare, file, and update a five year forecast on a fixed schedule. That forecast is not an optional planning exercise and it is not an internal management memo. It is the district’s primary public accounting document. By design, it shows how leadership models revenue, expenditures, cash balance, and deficit risk over time using standardized categories and disclosed assumptions. It exists so that financial claims made to the public can be tested against numbers rather than accepted on narrative authority.

The purpose of the five year forecast is to convert concern into calculation. It is where a district moves from a generalized statement such as “we may face a shortfall” to a definitive conclusion such as “we must reduce spending by eighteen million dollars annually.” That transformation does not occur rhetorically. It occurs through line items, assumptions, and projections that are visible by law and subject to public scrutiny. If Lorain City Schools is presenting the eighteen million dollar figure as a settled reality rather than a planning scenario, then the forecast behind it must already reflect that reality in plain numbers.

Baseline expenditures should be laid out clearly by function and object code, including salaries, benefits, purchased services, supplies, and capital outlay. Those figures are not merely descriptive. They show where costs are embedded, whether those costs are recurring, and whether growth occurred through negotiated agreements, benefit structures, staffing patterns, or administrative expansion. The revenue side of the forecast is equally critical. It should show projected state foundation funding, local property tax receipts, federal funding streams, and the distinction between restricted and unrestricted funds. That distinction matters because not all dollars are interchangeable. A projected deficit driven by restricted funds expiring raises fundamentally different policy questions than a deficit driven by unrestricted operating costs. Without seeing how each revenue source was modeled, the public cannot assess whether the shortfall reflects external constraint or internal choice. The assumptions section of the forecast is where credibility is ultimately earned or lost.

Enrollment projections, property valuation trends, negotiated wage increases, benefit cost growth, special education obligations, and transportation cost trends are not neutral inputs. They are judgment calls informed by data, expectations, and policy posture. Small changes in these assumptions can materially alter both the size and timing of a projected deficit.

If the district is confident enough to declare that eighteen million dollars in annual cuts is unavoidable, it should be confident enough to show the assumptions that made that conclusion inevitable. Finally, the forecast must show the cash balance trajectory. This is where urgency is either substantiated or exposed. The public should be able to see when the district is projected to cross into deficit spending, how quickly reserves are depleted, and precisely what level of reduction is necessary to prevent that outcome. If the eighteen million dollar figure is accurate, the forecast should demonstrate why a smaller reduction is insufficient and why a different mix of adjustments would fail. If the district cannot point the public directly to the forecast line items and assumptions that produce the eighteen million dollar conclusion, then it is not asking for understanding. It is asking for acceptance.

A headline number without underlying accounting is not transparency. It is persuasion.

Ohio’s forecast requirements exist precisely to prevent school districts from asking voters, staff, and families to accept life altering financial decisions without being shown the math that justifies them.

“Unexpected” funding reductions deserve dates, documents, and agency notices

Large numbers do not materialize without a paper trail

The superintendent’s letter asserts that within roughly a two month period last summer, Lorain City Schools experienced several unexpected and material funding reductions. The figures cited are substantial. Nearly nine hundred thousand dollars less per year in federal funding than anticipated. A four point one million dollar annual shortfall in state funding. Approximately one million dollars per year redirected by the Lorain County Commissioners. These are not marginal adjustments. They are the kind of changes that materially alter a district’s operating posture. They also do not occur in a vacuum. Funding at this scale moves through formal channels. It is accompanied by grant award notices, calculation sheets, legislative updates, and written communications from state or federal agencies. If these reductions occurred as described, the district did not learn about them by surprise phone call or informal conversation. It learned about them through documents that should still exist.

The claim of a nearly nine hundred thousand dollar annual reduction in federal funding raises immediate and specific questions that the letter does not answer. Which programs lost the money. Title I. Title II. IDEA. Other formula based grants. Was this reduction the result of temporary pandemic era funding expiring, funding that should never have been treated as recurring in the first place, or was it a reduction to ongoing allocations that the district had a reasonable basis to expect would continue. If the reduction occurred suddenly, what notice did the district receive, on what date, and from which federal or state administering agency. Those details are not ancillary. They determine whether the shortfall reflects an external shock or an internal planning failure. The asserted four point one million dollar annual shortfall in state funding demands the same level of specificity. State foundation funding in Ohio is calculated under law. It does not fluctuate randomly. Changes of that magnitude are typically driven by enrollment shifts, formula adjustments enacted through the state budget, valuation changes, or explicit policy decisions. Each of those causes is traceable.

If the funding formula changed, the change exists in statute, budget legislation, or official calculation documents issued by the state. If enrollment declined more sharply than projected, that decline should appear in the district’s own data and forecasts. If the district relied on projections that did not align with how the formula actually operates, the public deserves to know where and why that error occurred. The most consequential and least explained claim in the letter, however, is the assertion that approximately one million dollars per year was redirected by the Lorain County Commissioners. That statement carries political weight. It implies a discretionary local decision rather than a formula driven outcome. It suggests an identifiable act by elected officials that reduced school funding. Yet the letter provides no mechanism, no statutory reference, and no documentation to support the claim. If county commissioners redirected school funding, there should be a record. A resolution. A budget amendment. A notice citing authority. Board minutes reflecting the decision. Communications to affected districts explaining the change. Absent that paper trail, the claim functions less as disclosure and more as deflection. It introduces a political actor as the cause of harm without giving the public the information necessary to evaluate whether that attribution is accurate.

When a district invokes “unexpected” funding reductions to justify eighteen million dollars in annual cuts, it assumes the burden of proof. Dates matter. Documents matter. Agency notices matter. Without them, the community is left with numbers that sound authoritative but cannot be tested.

Transparency does not mean asserting that reductions occurred. It means showing when they occurred, how they were communicated, and whether they were truly unforeseeable or simply inconvenient to acknowledge earlier.

“Unexpected” Funding Reductions Deserve Dates, Documents, and Agency Notices

Large numbers do not materialize without a paper trail

The superintendent’s letter asserts that within roughly a two-month period last summer, Lorain City Schools experienced several unexpected and material funding reductions. The figures cited are substantial: nearly nine hundred thousand dollars less per year in federal funding than anticipated, a four point one million dollar annual shortfall in state funding, and approximately one million dollars per year redirected by the Lorain County Commissioners. These are not marginal adjustments. They are changes large enough to materially alter a district’s operating posture. They also do not occur in a vacuum. Funding at this scale moves through formal channels. It is accompanied by grant award notices, calculation worksheets, legislative updates, and written communications from state and federal agencies.

If these reductions occurred as described, the district did not learn about them through informal conversations or last-minute surprises. It learned about them through documents that should still exist and should be readily producible. The claimed reduction of nearly nine hundred thousand dollars per year in federal funding raises immediate and specific questions that the letter does not answer. Which programs lost the funding: Title I, Title II, IDEA, or other formula-based grants. Was this reduction the result of temporary pandemic-era funding expiring, funding that should never have been treated as recurring in the first place, or was it a reduction to ongoing allocations that the district had a reasonable basis to expect would continue. If the reduction occurred suddenly, what written notice did the district receive, on what date, and from which administering agency. Those details are not ancillary. They determine whether the shortfall reflects an external funding shock or an internal planning failure.

The asserted four point one million dollar annual shortfall in state funding demands the same level of specificity. State foundation funding in Ohio is calculated under law. It does not fluctuate randomly. Changes of that magnitude are typically driven by enrollment shifts, formula changes enacted through the state budget, valuation adjustments, or explicit policy decisions. Each of those causes is traceable. If the funding formula changed, the change exists in statute, budget legislation, or official calculation documents issued by the state. If enrollment declined more sharply than projected, that decline should appear in the district’s own enrollment data and forecasts. If the district relied on projections that did not align with how the formula actually operates, the public deserves to know where and why that disconnect occurred.

The most consequential and least explained claim in the letter, however, is the assertion that approximately one million dollars per year was redirected by the Lorain County Commissioners. That statement carries political weight. It implies a discretionary local decision rather than a formula-driven outcome. It suggests an identifiable act by elected officials that reduced funding otherwise available to the district. Yet the letter provides no mechanism, no statutory reference, and no documentation to support the claim. If county commissioners redirected school funding, there should be a record: a resolution, a budget amendment, a formal notice citing authority, board minutes reflecting the action, and communications to affected districts explaining what changed, why it changed, and when it would take effect.

Absent that paper trail, the claim functions less as disclosure and more as attribution without proof. It introduces a political actor as the cause of harm without giving the public the information necessary to evaluate whether that attribution is accurate. When a district invokes “unexpected” funding reductions to justify eighteen million dollars in annual cuts, it assumes the burden of proof. Dates matter. Documents matter. Agency notices matter. Transparency does not mean asserting that reductions occurred. It means showing when they occurred, how they were communicated, and whether they were truly unforeseeable or simply unacknowledged until they became inconvenient to ignore. It is also important to state clearly what this analysis does and does not claim. Based on prior reporting and publicly documented patterns in Lorain County governance, the superintendent’s assertion regarding the Lorain County Commissioners is not facially implausible. This publication has previously reported on county-level fiscal decisions, allocation practices, and discretionary reallocations that materially affected downstream entities, including schools, public safety, and human services. In that context, the claim that approximately one million dollars per year was redirected away from school funding fits within an established pattern of centralized fiscal decision-making under the banner of budget control.

But plausibility is not proof, and credibility does not reduce the obligation to disclose. It increases it. When a claim aligns with prior reporting, the standard for documentation rises rather than falls. A pattern does not substitute for a record. It heightens the public interest in seeing the mechanism, the dates, and the authority relied upon. County commissioners do not act in the abstract. They act through resolutions, budget amendments, allocation formulas, settlement distributions, and statutory interpretations that are memorialized in agendas, minutes, fiscal reports, and correspondence. If the commissioners exercised discretion that reduced funding available to Lorain City Schools, the legal and financial framework for that decision exists somewhere in writing.

If the district is relying on this commissioner action as a material component of its eighteen million dollar shortfall narrative, then the district is in the best position to produce the supporting documents. It would have received notice. It would have adjusted its forecasts. It would have referenced the change internally.

Producing that paper trail would not weaken the district’s position. It would strengthen it by converting a politically charged assertion into a verifiable fact.The danger is not in naming the commissioners. The danger is in naming them without showing the work. In an environment already marked by public distrust and fiscal fatigue, unsupported attribution risks being read as blame shifting even when the underlying concern is legitimate. Transparency requires more than being likely correct. It requires being demonstrably correct. And if prior reporting is accurate, the documents exist. If they exist, they should be produced.

The Levy Setup Is Persuasion, Not Disclosure

Preparing the audience without presenting the terms

The superintendent’s letter signals a levy this spring and states plainly that without additional support, deeper reductions will be required. That framing will be familiar to anyone who has watched school finance campaigns unfold in Ohio. It establishes urgency, links hardship to voter action, and positions the levy not as one option among many, but as the inevitable next step if the community wishes to avoid further harm. What it does not do is disclose the substance of what is being proposed. A levy is not an abstract concept and it is not a mood. It is a legal instrument with defined terms and measurable consequences. It has a dollar amount. It has a duration. It has a type, whether operating, permanent improvement, bond, or a combination. It has designated uses. It allocates funds across categories. It produces a calculable tax impact on homeowners at different valuation levels.

“A levy is not a feeling and it is not a slogan. It is a legal instrument with a price tag, and the public is entitled to see that price before being asked to absorb it.”

None of that information appears in the district’s message, even though the letter is clearly designed to condition the public for an upcoming ask. That omission matters because the district is not merely announcing a possibility. It is shaping expectations. By warning that deeper reductions will occur without additional support, Lorain City Schools is implicitly narrowing the range of acceptable responses before the public has been shown the choices.

That is persuasion, not disclosure.

It asks families and taxpayers to emotionally brace for a solution that has not yet been defined, let alone justified with numbers. Transparency at this stage would look very different. If the district is preparing the community for a levy, transparency means publishing the levy math now. It means disclosing the proposed amount, the length of the levy, and the type of levy under consideration. It means explaining what the funds would be used for and, just as importantly, what they would not be used for. It means showing how the revenue would be allocated between operating costs and permanent improvements. It also means providing projected taxpayer impacts by property value bracket so families can understand the personal cost alongside the claimed public benefit.

“When families are already absorbing property tax increases approaching one hundred percent, asking them to brace for a new levy without terms, numbers, or household impact is not transparency. It is financial conditioning without disclosure.”

That context is especially critical given recent county level property revaluations that dramatically increased assessed home values across Lorain County. For many homeowners, those reassessments did not result in marginal changes. They resulted in effective property tax increases approaching one hundred percent. In practical terms, that meant annual tax bills that were once approximately six hundred thirty four dollars increased by roughly twelve hundred dollars, before any new levy is even considered. When families are already absorbing that level of increase through revaluation alone, asking them to contemplate additional taxation without clear levy terms, defined uses, and precise household impact calculations is not transparency. It is financial conditioning without disclosure. Equally important, transparency requires context. The public cannot evaluate a levy without seeing what was tried first and what alternatives remain.

Were all non instructional expenditures examined. Were administrative costs reduced proportionally. Were staffing models adjusted at the top as well as the classroom. Were program consolidations considered before permanent reductions.How much of the claimed deficit is driven by structural decisions that could be revisited without voter dollars.Those questions are not obstacles to a levy. They are prerequisites to informed consent.

Listening sessions held without this information risk becoming persuasion tours rather than deliberative forums.

They invite the public to react to consequences while withholding the decision tree that produced them. In that setting, feedback is necessarily constrained. Families are asked how they feel about cuts, not whether the proposed financial path is the only or best one available. If the district believes a levy is necessary, the strongest case it can make is a complete one. That means showing the math, the options matrix, and the tradeoffs before the ask is formalized. Anything less asks the public to commit emotionally and financially to a solution that has been framed, but not fully revealed.

The Staff Language Is Careful for a Reason, and the Community Should Be Careful Too

Reassurance can coexist with opacity

The superintendent’s letter includes a carefully constructed assurance regarding staffing. It promises that there will be no staff reductions before the end of the current school year except through attrition, and it states that affected individuals will be notified directly when reductions in force become necessary. On its face, the language is calming. It is designed to steady employees, reduce immediate fear, and prevent disruption in classrooms during the remainder of the year. As communication, it is effective. As disclosure, it is incomplete.

That careful wording also creates a temporal buffer. By drawing a firm line at the end of the school year, the district preserves a period in which modeling, scenario building, and internal decision making can proceed without public scrutiny.

During that window, leadership can evaluate which buildings may be consolidated, which programs may be reduced or eliminated, and which job classifications are most vulnerable, all while the broader community is told that nothing is happening yet. The absence of immediate action does not mean the absence of planning. In practice, it usually signals the opposite. If Lorain City Schools is already modeling staffing cuts, consolidations, and program reductions as part of its response to the claimed eighteen million dollar shortfall, then those models exist now. They do not appear suddenly on the day notices are issued. They are built in advance through enrollment projections, staffing ratios, budget scenarios, and internal spreadsheets. Waiting until decisions are final does not preserve transparency. It forecloses it. Transparency in this context does not require naming individual employees or issuing premature notices. It requires disclosing categories and scenarios.

Which grade bands are being evaluated for consolidation?

Which buildings are under review?

Which programs are considered discretionary versus essential?

Which job classifications are being modeled for reduction and on what basis?

Without that information, the community is asked to absorb outcomes without being allowed to understand or test the reasoning that produced them.

When leadership invokes transparency while withholding the analytical framework guiding its choices, transparency becomes a slogan rather than a practice. It sells patience rather than participation. Families, staff, and taxpayers are asked to trust that decisions will be fair and necessary, even though they are not given access to the criteria by which fairness and necessity are being judged. Careful language can be humane. It can also be strategic. The community should be capable of holding both truths at once. Reassurance about timing does not eliminate the need for disclosure about direction. If the district believes its staffing plans will withstand public scrutiny, the most credible way to demonstrate that confidence is to share the categories, assumptions, and scenarios now, while there is still time for meaningful input, rather than after choices have hardened into inevitability.

Administrative Structure, Salary Concentration, and Why Staffing Cuts Rarely Begin at the Top

Patterns of insulation matter more than individual résumés and the district’s assurances around staffing cannot be evaluated in isolation from its broader administrative structure or governance culture. Lorain City Schools operates within a local government ecosystem where a consistent pattern has emerged over years of reporting and public records analysis. Administrative layers are preserved. Director level roles proliferate. Salaries above ninety thousand dollars become normalized. When fiscal pressure arrives, austerity is applied downstream. This pattern is not unique to the school district. It mirrors what has occurred across Lorain city and county government, where management positions remain comparatively insulated while frontline workers absorb instability. Lorain City Schools reflects that same structural posture.

Classroom teachers, paraprofessionals, aides, and support staff experience recurring cycles of uncertainty. Meanwhile, the upper tiers of administration remain largely intact. Titles shift. Departments are rebranded. New leadership roles appear or existing ones are elevated. Compensation at the top remains comparatively stable even as instructional environments face disruption. That reality shapes how staff receive assurances that no reductions will occur yet.

The issue is not whether administrators deserve fair compensation. It is proportionality, sequencing, and credibility. When a district warns of deep cuts while maintaining a top heavy structure, staff skepticism is not cynicism. It is informed by experience. Employees understand that staffing models historically do not begin with executive roles. They begin with those least protected and least insulated from decision makers.

This skepticism is intensified when administrative hiring and compensation decisions occur during the same period the district is messaging austerity. When leadership positions remain protected or expanded while staff are told to brace for layoffs, the implicit message is not reassurance. It is hierarchy.

This article does not attempt to adjudicate the merits of any individual administrator’s résumé. That analysis belongs in a separate examination of how leadership roles are filled, validated, and insulated from influence within the district. What matters here is the structural signal being sent. When austerity flows downward but compensation and job security remain concentrated at the top, promises about timing do little to rebuild trust.

If Lorain City Schools wants its staffing language to be received as good faith rather than strategic delay, it must address this imbalance directly. That means explaining whether administrative structure itself is part of the solution or treated as untouchable. It means disclosing where modeling has begun, not merely when outcomes will be announced. Without that clarity, assurances ask patience from those who have historically been asked to sacrifice first.

The Ballard Connection, Communications Pay, and Why Process Matters More Than the Number

When governance overlap replaces insulation, credibility erodes. Context matters when discussing compensation. As of early 2026, statewide data shows that Director of Communications salaries in Ohio frequently fall between seventy thousand and one hundred twenty thousand dollars, with higher compensation appearing in larger or more complex organizations. On paper, a salary near ninety thousand dollars for a senior communications role is not inherently improper. But market averages answer only one question. What such roles can pay. They do not answer why this role pays what it does in this district, at this moment, under this governance structure, and through what process.

Lorain City Schools has long treated communications as a senior administrative function. Prior occupants of high level communications roles were compensated accordingly. The issue here is not that communications has never been paid well. It has.

What has changed is the governance context surrounding the position and the concentration of familial relationships within district administration.

The current Director of Communications and Community Relations is the daughter of a sitting board member. That same board member’s spouse is also employed by the district in an administrative capacity, working in student facing operational domains. Together, these relationships place multiple immediate family members of a governing official inside the district’s administrative structure at the same time.

This fact alone does not establish misconduct. But it does fundamentally alter the governance analysis. The board member in question participates in oversight structures that intersect with staffing, institutional culture, and communications posture. At the same time, the district is telling staff and families that it faces an unavoidable eighteen million dollar annual shortfall, that layoffs are likely, and that austerity must be absorbed across the system.

This is where salary comparisons cease to be dispositive. Paying a communications director a market rate salary is defensible when the district can demonstrate that the position was filled through a fully insulated, competitive process that was meaningfully independent of board influence. It is defensible when recusals are documented, when selection criteria are disclosed, and when governance relationships are clearly separated from hiring authority. It is defensible when administrative roles are scrutinized with the same rigor applied to classrooms and support staff during periods of fiscal stress. What undermines confidence is not the existence of a well compensated communications role. It is the absence of publicly available documentation showing that this particular hire was insulated from governance proximity, especially where immediate family members of a board member occupy multiple administrative positions within the same institution.

Ohio ethics standards do not hinge on whether a salary falls within a market range. They hinge on whether a benefit would have occurred but for access, position, or influence, and whether the process was meaningfully independent and documented. The presence of multiple familial ties heightens, rather than diminishes, the obligation to show insulation through records. That concern is amplified by timing. The continued protection of senior administrative roles connected by family relationship to governance occurred as the district intensified austerity messaging and levy preparation. Employees and taxpayers do not evaluate that sequence abstractly. They evaluate it against what they are being asked to give up.

This article does not attempt to fully compare the qualifications, experience, or validation pathways of current and prior communications leadership. That analysis requires a separate, detailed examination of hiring pipelines, reference structures, and the roles played by senior decision makers. A forthcoming piece will examine those dynamics directly.

For purposes of this analysis, the issue is governance integrity. If the district believes this hire and administrative structure reflect best practice, the response is straightforward. Produce the records. Show the posting. Show the applicant pool. Show the scoring. Show the recusals. Show that the outcomes were insulated from influence and would have occurred regardless of family relationship. Until then, the question is not whether the salary fits within an Ohio average.

The question is whether, in a declared financial emergency, the rules were applied evenly, visibly, and credibly. That question cannot be answered with tone or reassurance. It can only be answered with documents.

What Transparency Looks Like Under Ohio Public Records Law

Disclosure is the test, not intent. If district leadership is sincere in its repeated invocation of transparency, the next step is not another carefully worded letter or another round of listening sessions. The next step is disclosure. Ohio law does not measure transparency by tone, reassurance, or stated values. It measures it by access to records.

Ohio Revised Code 149.43 guarantees the public the right to inspect and copy public records. That right exists precisely so that major financial claims, particularly those used to justify layoffs, consolidations, and tax levies, can be independently verified. When a school district asserts that it must reduce spending by eighteen million dollars annually, the records that produced that conclusion are not optional. They already exist if the claim is accurate. At a minimum, transparency requires that the district make available the most recent five year forecast relied upon in reaching the eighteen million dollar figure, including the assumptions worksheets and any internal schedules used to model revenue, expenditures, and cash balance. The forecast is not a summary document. It is the legal backbone of district financial planning, and without the assumptions that drive it, the numbers cannot be meaningfully evaluated. Transparency also requires disclosure of any correspondence or formal notices from federal or state agencies documenting the funding reductions described in the superintendent’s letter. That includes written notifications identifying which programs were affected, the effective dates of the reductions, and the authority under which those changes occurred. Large funding shifts do not occur without documentation, and the public is entitled to see it.

If the district has engaged with the Ohio Department of Education and Workforce regarding deficit conditions, corrective action, or fiscal oversight, those communications are likewise public records. Such correspondence would help the community understand whether the district’s current posture reflects regulatory requirements, advisory guidance, or internal decision making framed as inevitability. The district has also stated that it spent months reviewing its budget and preparing for the reductions now being announced. That process necessarily generated internal documents. Budget reduction scenarios, staffing models, program evaluations, consolidation analyses, and financial projections do not exist only in leadership discussions. They exist on paper and in digital form. Those materials are public records to the extent they document official functions and decision making. Finally, if approximately one million dollars per year was redirected as a result of county level action, any communications, resolutions, budget amendments, or formal notices involving the Lorain County Commissioners that support that claim must exist somewhere in writing. Producing those records would clarify not only whether the assertion is accurate, but how it fits into the district’s broader financial picture.

Transparency is not about asking the public to trust that leadership has done the work. It is about allowing the public to see the work for itself. Ohio’s public records law exists to prevent exactly this kind of moment from turning into a test of faith. When decisions of this magnitude are presented as unavoidable, the records that produced them must be visible. If leadership wants to be believed, leadership should be willing to show the public what it relied upon to reach its conclusions. Anything less is not transparency. It is expectation management.

Final Thought

The bottom line is not tone. It is proof. The superintendent asked the community to hear directly from the district. That is a fair request. Public institutions should speak for themselves, and leadership should not have to communicate through rumor or speculation. But that request runs both ways. If the district expects to be heard, it also has an obligation to listen to what the public is asking for in return.

What the community is asking for is not reassurance. It is not optimism. It is not another round of listening sessions framed around outcomes that have already been decided. It is records, context, and honesty about how we got here.

That context matters because Lorain City Schools is not just facing a budget problem. It is facing an outcomes problem. Academic performance has remained near the bottom of state rankings for years. Enrollment has continued to decline. Families with means have voted with their feet. And yet, through all of this, administrative layers have multiplied rather than contracted. Titles have expanded. Director level positions have become routine. Salaries above ninety thousand dollars have been normalized at the top, even as classroom resources, staffing stability, and student outcomes have failed to materially improve. That imbalance cannot be ignored when the district asks for sacrifice.

It also cannot be ignored when the district maintains a leadership structure that would raise questions in any environment, let alone a declared financial emergency. Lorain City Schools currently operates with multiple superintendent level roles. Families and taxpayers are entitled to ask why. What distinct functions justify three superintendent titles. What responsibilities cannot be consolidated. What outcomes those layers have produced. And why, if eighteen million dollars in annual cuts are unavoidable, structural leadership reform is not being discussed with the same urgency as classroom level reductions. These are not rhetorical questions. They are governance questions. And they go directly to whether austerity is being shared or managed downward.

If Lorain City Schools is going to tell families, staff, and taxpayers that eighteen million dollars in annual cuts is unavoidable, then the district should be willing to put the underlying work on the table. Publish the five year forecast that produces that number. Publish the assumptions that make the deficit inevitable rather than contingent. Publish the federal and state notices that document the claimed funding reductions. Publish the internal models and scenarios that were built during the months of review leadership says it undertook. Publish the documents that explain how this path was chosen over others, including whether administrative structure and executive compensation were meaningfully evaluated as part of the solution. Do it before the levy language is finalized. Do it before staffing decisions harden into notifications. Do it before consolidation plans are framed as the only responsible option left.

Transparency after decisions are locked in is not transparency. It is post hoc justification.

This matters for another reason as well. The district is not operating in a vacuum. Personnel decisions, administrative structure, compensation priorities, and governance relationships all shape how austerity claims are received by the people who are being asked to absorb the consequences. A separate piece now in production will examine those dynamics more closely, including how specific roles, relationships, and decision makers fit into the broader picture being presented here. That work exists because trust is built on context, not messaging.

“Stay Titan Strong” may be an effective rallying phrase.

It may steady nerves.

It may signal resilience.

But it is NOT a financial strategy, and it is NOT a substitute for disclosure.

The people of Lorain do not owe blind trust to any institution that ranks near the bottom in outcomes, maintains a top heavy administrative structure, and then asks for new taxes while cutting from the classroom outward. What they are owed, under Ohio law and basic principles of accountable governance, is access to the records that justify those demands.

Show the math. Show the structure. Show the choices. Then, and only then, ask the public to carry the weight.

Legal and Editorial Disclosures

This article is published by Aaron Knapp in his capacity as an investigative journalist and commentator. It reflects analysis, interpretation, and opinion based on publicly stated claims, public records, firsthand knowledge, and contemporaneous reporting. Any factual assertions are intended to be grounded in verifiable documentation or direct observation. Readers are encouraged to review original source materials where available and to draw their own conclusions.

Nothing in this publication constitutes legal advice, nor does anything herein create an attorney–client relationship. This article is provided for informational, journalistic, and commentary purposes only. Readers seeking legal advice regarding a specific matter should consult a licensed attorney of their choosing.

This story is published in good faith. If a material factual error is identified and supported by reliable documentation, a correction will be considered and, where appropriate, published.

Where this article discusses public institutions, public officials, or matters of governance, it is intended as fair comment on issues of public concern. References to individuals or entities are made solely in connection with reporting, analysis, and accountability journalism.

Artificial Intelligence Disclosure

Portions of this article were drafted, edited, or refined with the assistance of artificial intelligence tools used as a writing and research aid. All final content decisions, factual assertions, framing, and editorial judgments were made by the author. AI tools were not used to fabricate sources, documents, quotations, or legal authorities.

LLC Limitation and Liability Notice

This publication is issued through Knapp Unplugged Media LLC for investigative journalism and commentary purposes. Content is provided “as is” for public information and discussion. To the fullest extent permitted by law, Knapp Unplugged Media LLC disclaims liability for actions taken by readers based on information or commentary contained in this publication.

© 2026 Knapp Unplugged Media LLC. All rights reserved. No portion of this publication may be reproduced, redistributed, or republished without prior written permission, except for brief quotations used for news reporting, criticism, or commentary consistent with fair use.