An UnPlugged Exclusive: A Statement That Carries Institutional Weight, Not Personal Opinion

How a single sentence issued under color of office locked Lorain County into a question it can no longer evade, reported exclusively by Unplugged Media

By Aaron Knapp

Investigative Journalist

Publisher, Unplugged with Aaron Knapp

Contributing reporting by Garon Petty

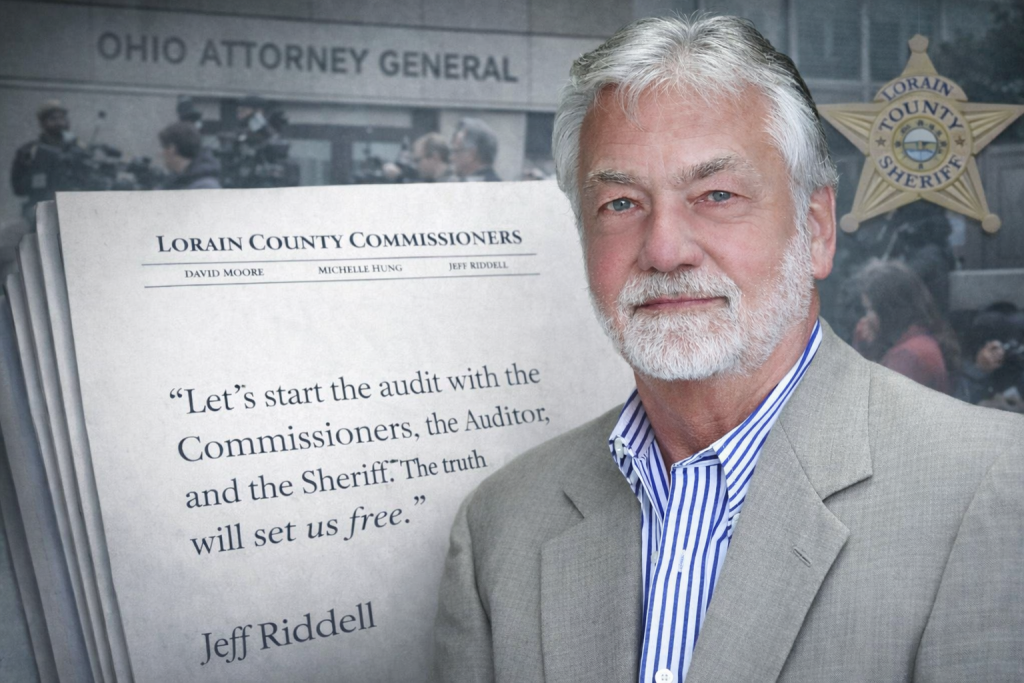

When Jeff Riddell wrote, “Let’s start the audit with the Commissioners, the Auditor, and the Sheriff. The truth will set us free,” he did not do so in a casual or ambiguous setting. This was not a social media post dashed off in the heat of an argument. It was not an unscripted remark at a public meeting that could later be dismissed as rhetorical excess or imprecise language. It was not sent from a personal email account or framed as an individual opinion detached from office. It was written on official Lorain County Commissioners letterhead and transmitted to a broad and deliberate audience that included journalists, senior state officials, the Ohio Attorney General, and the Lorain County Sheriff himself. That context is not incidental. It is determinative.

“Let’s start the audit with the Commissioners, the Auditor, and the Sheriff. The truth will set us free.”

Government letterhead is not decorative. It is a formal signal that the speaker is acting in an official capacity and invoking the authority of the office they hold. When an elected county commissioner communicates on official stationery, the message is presumed to reflect institutional posture, not private commentary. The choice to use letterhead transforms the content of the message from opinion into record. It tells recipients, including oversight bodies and the public, that the statement is being made with the weight of office behind it and with the understanding that it may be relied upon as an expression of governmental position.

This distinction is not academic. Courts, auditors, inspectors general, and investigative bodies routinely differentiate between personal remarks and official communications when assessing intent, knowledge, and accountability. An email sent on government letterhead is treated as an act of governance. It becomes part of the documentary trail that defines what officials knew, what they acknowledged, and how they framed their responsibilities at a given moment in time. By choosing that medium, Riddell crossed a clear line from political rhetoric into institutional declaration.

In this case, the institution being invoked is the Lorain County Board of Commissioners. Once that authority is engaged, the statement no longer belongs solely to the individual who wrote it. It attaches to the office and, by extension, to the governing body itself. That is why such communications are preserved, requested, and scrutinized in audits and investigations. They are treated as evidence of official posture, not as passing commentary.

The practical consequence is simple but profound. By placing this language on commissioners letterhead, Riddell ensured that it entered the public record of county governance. It is now a fixed point that cannot be quietly walked back, reframed as metaphor, or dismissed as personal bravado. It stands as a formal acknowledgment, issued under color of office, that an audit is appropriate and that multiple branches of county government are proper subjects of review. At that moment, the statement ceased to be a rhetorical flourish and became a documented act of public administration.

Anchoring the Audit Comment in a Broader Pattern of County Governance Issues

The moment Commissioner Riddell issued his audit invitation on official letterhead did not occur in isolation. It came against a backdrop of months of investigative coverage by Unplugged Media documenting long-running disputes over budget transparency, resistance to public records disclosures, and contested accounting practices within Lorain County government. Stories such as “Their Decisions Have Put the Lorain County Population at Risk” and “Why I Filed Formal Complaints With the Sheriff, the Attorney General, and the Chronicle-Telegram” chart a distinct pattern in which county officials have routinely clashed with journalists, oversight bodies, and citizens over access to financial information and the interpretation of official duties.

Why the Phrase “Let’s Start the Audit” Is an Admission, Not a Challenge

The operative word in Jeff Riddell’s sentence is not “truth.” It is “audit.” That distinction is critical because audits are not rhetorical devices and they are not used to swat away imaginary problems. An audit is a formal accountability mechanism. It is initiated when there is a legitimate question about financial practices, compliance with law, internal controls, or the allocation of responsibility across offices. By explicitly calling for an audit and by naming its scope as “the Commissioners, the Auditor, and the Sheriff,” Jeff Riddell did something far more consequential than challenge a narrative. He acknowledged that the issue at hand is structural in nature and not reducible to personality, politics, or messaging.

The operative word is not “truth.” It is “audit.”

That acknowledgment matters because it directly conflicts with the commissioners’ earlier framing of the fleet controversy as a “manufactured issue.” Those two positions cannot logically coexist. A manufactured issue collapses under routine documentation. If the facts are false or exaggerated, the remedy is simple. You produce the payment records, the lease terms, and the correspondence showing compliance, and the matter ends. You do not initiate a multi office audit to disprove fiction. You initiate an audit when the facts are either unclear, disputed, or indicative of deeper systemic problems that cannot be resolved by pointing to a single spreadsheet.

An audit is not theater. It is a concession that ordinary explanations are insufficient. It is a recognition that the normal channels of assurance have failed or been called into question. By invoking that process, Riddell implicitly conceded that the controversy could not be resolved through public relations alone and that the available documentation, at least as publicly presented, did not definitively settle the matter.

The inclusion of his own office within the proposed audit scope is especially telling. Public officials do not casually invite scrutiny of themselves unless they understand that responsibility is shared or entangled. By naming the Commissioners alongside the Auditor and the Sheriff, Riddell acknowledged that the chain of accountability runs through multiple offices and decision points. That framing undermines any attempt to isolate blame to a single department or to dismiss the deputies union’s statements as irrelevant or false without examination.

Whether intentional or not, the statement functions as an admission that the fleet controversy implicates budgetary authority, oversight responsibilities, and inter office coordination. It recognizes that payment failures, if they occurred, did not happen in a vacuum and that resolving the question requires tracing decisions across institutional boundaries. Once that admission is made on the record, it cannot be recharacterized as mere bravado or rhetorical confidence. It becomes a recognition that the problem is real enough to warrant formal review.

In that sense, “Let’s start the audit” is not a dare. It is an acknowledgment. It concedes uncertainty where certainty had been publicly claimed and replaces narrative dismissal with procedural accountability. From that moment forward, the issue ceased to be about who was exaggerating and became about what the records will ultimately show.

The Scope He Named Is the Story

Jeff Riddell did not say, “Audit the Sheriff.” He did not say, “Audit the union.” He did not attempt to cabin the controversy within a single office or redirect scrutiny toward a politically convenient target. Instead, Jeff Riddell explicitly stated that the audit should begin with the Commissioners, the Auditor, and the Sheriff. That choice of scope is not incidental language. It is the substance of the statement itself. By defining the starting point this way, Riddell signaled that the controversy necessarily implicates decision making authority, budget control, and institutional oversight across multiple centers of county power.

The scope becomes the story, and the story becomes one of institutional accountability rather than individual fault.

If responsibility for non payment or mismanagement of fleet leases truly rested with the sheriff alone, there would be no rational or procedural justification for including the commissioners or the auditor at the outset. In such a scenario, the inquiry would be narrow and administrative. It would examine whether the sheriff’s office failed to process payments, misallocated funds, or ignored contractual obligations. The matter would rise or fall on those records alone. Expanding the scope beyond that framework is an acknowledgment that the issue cannot be resolved by isolating one department.

The commissioners control appropriations. They approve budgets, set spending priorities, and exercise fiscal oversight over county departments. Their inclusion in the audit scope concedes that questions may exist about how funds were allocated, whether appropriations were sufficient or timely, and how financial responsibilities were communicated between offices. That is not a sheriff only problem. It is a governance question.

The inclusion of the Lorain County Auditor is even more revealing. Auditors are not political referees and they are not summoned to adjudicate narrative disputes. Their function is technical, statutory, and document driven. They examine whether funds were lawfully appropriated, properly disbursed, accurately tracked, and transparently reported in accordance with law and policy. They assess internal controls, compliance failures, and breakdowns in fiscal accountability. When an elected official invokes the auditor, it is an acknowledgment that the controversy turns on accounting reality rather than public messaging.

By naming the auditor alongside the commissioners and the sheriff, Riddell implicitly recognized that the core questions involve who authorized spending, who controlled the flow of funds, who bore responsibility for payment execution, and who was obligated to detect and correct deficiencies when payments were not made. Those questions cannot be answered through press statements or rhetorical blame shifting. They require reconstruction of the financial trail across offices and across time.

This scope also directly undermines any effort to portray the fleet controversy as a simple dispute over narrative or a manufactured issue inflated by outside actors. Manufactured issues do not require auditors. They require clarification. Audits are reserved for situations where the records themselves must be examined because responsibility is distributed and the answers are not self evident.

In that sense, the scope Riddell named reframes the entire controversy. It shifts the question from whether one office failed to pay its bills to whether Lorain County’s fiscal systems, oversight mechanisms, and inter office coordination functioned as required. Once that framing is placed on the record by a sitting commissioner, it cannot be undone. The scope becomes the story, and the story becomes one of institutional accountability rather than individual fault.

Why These Questions Matter and Why Their Source Matters

The questions that framed this exchange did not arise in a vacuum. They were posed by Garon Petty, a contributing author to Unplugged Media, and they were directed outward to elected officials, oversight bodies, and the press precisely because they implicate public accountability rather than private grievance. That context is important because it clarifies intent. These were not partisan talking points or adversarial provocations. They were substantive questions grounded in observable facts and raised in the course of civic inquiry.

When a citizen journalist and contributor poses questions about public spending and receives an on letterhead response from a sitting commissioner calling for an audit of multiple county offices, the interaction crosses from commentary into governance.

Petty’s role as a contributing author is relevant here not as a credential for authority but as evidence of purpose. The questions were framed for public understanding and public scrutiny. They were designed to force clarity on who controls county finances, who bears responsibility for payment failures, and how oversight mechanisms function when multiple offices intersect. In other words, they were the type of questions auditors, inspectors, and journalists routinely ask when fiscal narratives diverge.

That framing undercuts any attempt to dismiss the exchange as noise or agitation. When a citizen journalist and contributor poses questions about public spending and receives an on letterhead response from a sitting commissioner calling for an audit of multiple county offices, the interaction crosses from commentary into governance. The response did not deflect or decline to answer. It escalated. It acknowledged the legitimacy of the inquiry by proposing formal review.

This distinction matters because it fixes the origin of the audit discussion. The call for scrutiny did not emerge spontaneously from within the commissioners’ office as a proactive transparency initiative. It was elicited by external questioning from a contributor operating in a journalistic capacity. That sequence reinforces the conclusion that the issue demanded more than a dismissive label like “manufactured.” It required engagement at an institutional level.

In that light, Petty’s questions function as the catalyst that exposed an internal contradiction. They prompted a response that simultaneously sought to project confidence while conceding the need for formal examination. That contradiction is not attributable to the questioner. It is embedded in the official reply. Once the county chose to answer a journalist’s inquiry with an audit invitation on official letterhead, the matter ceased to be a debate over narrative and became a documented moment of public accountability.

Letterhead Turns Narrative Control Into Evidentiary Record

There is a sharp and consequential difference between aggressive rhetoric and an official written statement, and that difference is what gives this email its lasting legal and institutional significance. When this response was issued on commissioners letterhead, it ceased to be a moment of political positioning and became a timestamped governmental record. From that point forward, the statement entered the universe of documents that auditors, investigators, and courts rely upon to determine what public officials acknowledged, when they acknowledged it, and how they framed their responsibilities at the time.

That is the risk inherent in communicating on official letterhead. It converts narrative control into evidentiary footprint.

That transformation carries concrete consequences. If a comprehensive audit is later resisted, delayed, or narrowed in scope, this statement will stand as documentary evidence that a sitting commissioner publicly invited broad scrutiny of county finances and oversight. It directly undercuts any future claim that calls for review were unexpected, reckless, or driven by outside agitation. The invitation already exists in the record, issued under the authority of office. It cannot be credibly denied, minimized, or recharacterized as hypothetical once it has been formally made.

If, on the other hand, an audit proceeds and uncovers discrepancies, lapses in internal controls, or failures in payment and oversight, the same statement will assume an even heavier evidentiary role. It will demonstrate that county leadership was aware, in advance, that formal scrutiny was appropriate. In that context, the language “Let’s start the audit” will not be read as bravado or confidence. It will be read as acknowledgment. Investigators and auditors will treat it as proof that the need for examination was recognized at the time, regardless of whether subsequent actions aligned with that recognition.

Public officials often underestimate how their words age. Statements made during controversy do not fade when the headlines move on. They persist in public records systems, email archives, and investigative files. When they resurface months or years later, they are stripped of tone, posture, and political context. What remains is the substance. What was conceded. What was invited. What was placed within the reasonable expectation of oversight.

That is the risk inherent in communicating on official letterhead. It converts narrative control into evidentiary footprint. In this case, it fixed a point in the public record against which all subsequent actions will be measured. Whether Lorain County ultimately embraces scrutiny or retreats from it, this email will continue to speak. It will do so not as commentary and not as opinion, but as evidence of what county leadership acknowledged when the question of accountability was placed squarely before it.

The Broader Context Makes the Risk Obvious

This comment does not exist in isolation, and treating it as a standalone moment would miss why it is so consequential. Lorain County has spent the last several years mired in recurring financial disputes, contested narratives about accounting and budgeting, rejected or questioned audits, and repeated resistance to outside review when scrutiny intensified. Those patterns form the backdrop against which Riddell’s audit invitation must be read. In a county with a clean and uncontroversial fiscal record, such a statement might register as routine transparency. In Lorain County, it functions very differently.

Against that history, an open invitation to audit operates simultaneously as a dare and a liability. It raises expectations not only among the public but among watchdog entities, auditors, journalists, and oversight officials who have already seen previous efforts to limit, delay, or reframe financial review. Once a sitting commissioner publicly signals that an audit should begin and identifies multiple offices as appropriate subjects, the burden shifts. The expectation becomes that scrutiny will follow, not that the controversy will be managed away through messaging.

That is where the risk sharpens. If no audit occurs, the question is no longer whether the fleet issue was manufactured. The question becomes why an audit publicly invited by a commissioner never materialized. Silence or inaction in that scenario invites inference. It suggests either that the invitation was not sincere or that the findings were unwelcome. In a county already criticized for opacity, that absence becomes its own form of evidence.

If an audit does occur and confirms deficiencies, gaps in oversight, or failures in internal controls, the earlier effort to characterize the issue as manufactured will age poorly. What may have been framed as confidence will read, in hindsight, as deflection. Statements meant to minimize concern will be reinterpreted as attempts to manage perception before the records were examined. That is not speculation. It is how audit narratives are constructed once documentation replaces rhetoric.

Either outcome carries consequence. An audit that never happens undermines credibility and reinforces suspicions of avoidance. An audit that proceeds and uncovers problems validates the underlying concern and reframes earlier dismissals as premature or misleading. In both cases, the risk was created the moment the audit was invited on the record. That is why this comment matters so deeply. It locked Lorain County into a trajectory where accountability could no longer be safely postponed or selectively applied without raising new and more damaging questions.

Why This Cannot Be Walked Back Quietly

Once an elected official calls for an audit on official letterhead and circulates that call to state level oversight bodies, the statement cannot be unspoken. It cannot be softened after the fact or reframed as casual rhetoric. The record exists. Any subsequent effort to minimize, delay, or redefine the scope of review will be evaluated against that explicit invitation. What was publicly offered becomes the baseline against which later conduct is measured.

That is especially true here because the statement was not limited to a procedural suggestion. The phrase “The truth will set us free” elevates the commitment from administrative housekeeping to an affirmative embrace of transparency. It frames openness as a value voluntarily asserted by leadership, not as an obligation imposed by outside pressure. By using that language, the author of the statement placed moral and institutional weight behind the call for review.

Once transparency is invoked as a virtue on the record, abandoning it becomes far more costly than never having promised it at all.

Auditors and investigators pay close attention to that kind of framing. It does not deter inquiry. It invites it. When officials publicly assert that scrutiny will lead to truth and resolution, oversight bodies treat that assertion as an acknowledgement that review is appropriate and welcome. It becomes part of the justification for examination, not a reason to hesitate.

If subsequent actions contradict that framing through delay, resistance, or selective narrowing of scope, the contrast becomes evidence in itself. Investigators do not evaluate only what officials say in isolation. They assess consistency between words and actions over time. In that assessment, a public call for audit followed by retreat carries its own implications.

This is why the statement cannot be quietly walked back. It fixed expectations. It signaled readiness for scrutiny. Any departure from that signal will not go unnoticed, particularly in a county already under heightened attention for financial governance. Once transparency is invoked as a virtue on the record, abandoning it becomes far more costly than never having promised it at all.

The Bottom Line

Jeff Riddell’s audit comment was not casual, not rhetorical, and not harmless. It was an official acknowledgment that the fleet controversy reaches across multiple centers of authority within Lorain County government and warrants formal examination. By placing that acknowledgment on commissioners letterhead, Jeff Riddell transformed what might otherwise have been dismissed as political messaging into an institutional record with enduring consequence.

That act matters because official records do not exist in isolation. They become reference points. They are weighed against subsequent conduct, invoked in oversight inquiries, and revisited when questions of accountability resurface. In this case, the statement fixed a clear moment in time when a sitting commissioner publicly recognized that scrutiny was appropriate and that responsibility could not be confined to a single office.

From this point forward, the story is no longer about who said what in the heat of a dispute or whose rhetoric was sharper in a public exchange. It is about whether Lorain County will honor its own invitation to transparency or attempt to retreat from it once the attention shifts. That question cannot be answered by press releases or deflection. It can only be answered by action and by records.

Those records will decide which path was taken. They will show whether an audit was pursued, resisted, narrowed, or abandoned. And long after the email thread itself fades from public view, the documentary trail created by this statement will remain. It will continue to speak, not in the language of politics, but in the language of accountability.

A Necessary Acknowledgment of Persistence and Civic Pressure

It is also important to be clear about how this moment came into existence and who forced it into the open. This audit language did not originate from within county leadership as a voluntary transparency initiative. It was elicited. It came in response to persistent questioning by Garon Petty, a contributing author to Unplugged Media, who refused to accept dismissal, deflection, or narrative framing as substitutes for answers. His questions were not casual. They were directed, repeated, and grounded in the basic premise that public money and public safety demand public explanation.

This moment exists because Garon Petty refused to let the issue be waved away.

Petty’s persistence matters because it demonstrates how accountability pressure actually works in practice. The county did not wake up one morning and decide to invite an audit. The invitation was extracted through sustained inquiry that left officials with fewer rhetorical exits. When faced with questions that could not be neutralized by labeling the issue “manufactured,” a sitting commissioner responded on official letterhead with language that explicitly authorized scrutiny. That is not coincidence. That is cause and effect.

In practical terms, Petty’s work did more than raise awareness. It compelled an institutional response. By continuing to press, by copying oversight bodies and media, and by framing the issue in terms of fiscal responsibility rather than political conflict, he narrowed the space for dismissal. The result was an on the record statement that now binds the county to its own words. Whether or not an audit ultimately proceeds, the authorization exists because the questioning did not stop when the answers proved uncomfortable.

That contribution deserves recognition because it underscores a larger truth about local accountability journalism. Oversight is rarely offered freely. It is usually demanded, often repeatedly, by people willing to be labeled inconvenient. In this case, persistence produced paper. And paper, especially when it carries county letterhead, outlives spin.

This story is therefore not only about what Jeff Riddell wrote. It is also about why he wrote it and under what pressure. Without sustained inquiry from outside the halls of power, this moment would not exist in the record. That fact reinforces the broader theme running through this and other county reporting. Accountability in Lorain County has not been absent because no one asked. It has been absent because asking has too often been treated as provocation rather than civic duty.

Here, the asking worked. And that alone makes this moment worth documenting.

Final Thought

Accountability Does Not Appear Spontaneously. It Is Forced Into the Record.

Nothing about this moment was accidental, and nothing about it should be treated as routine. Jeff Riddell’s audit comment did not emerge from a sudden embrace of transparency or a proactive commitment to oversight. It emerged because persistent questioning made narrative control untenable. That distinction matters, and it sits at the core of nearly every county story I have reported over the last several years.

Again and again, Lorain County governance follows the same arc. A concern is raised. It is dismissed as manufactured, exaggerated, or politically motivated. Records are slow walked or withheld. Oversight is framed as harassment. Then, when pressure builds and the questions do not go away, the posture shifts. Transparency is suddenly invoked, often rhetorically first, procedurally later if at all. What changes the dynamic is not goodwill. It is documentation.

This audit authorization fits squarely into that pattern. The fleet controversy was not treated as serious until it could no longer be contained through messaging. Once the conversation escaped the bounds of talking points and entered the realm of documented inquiry, the response escalated. The result was an on the record statement, on county letterhead, calling for an audit that explicitly included the Commissioners, the Auditor, and the Sheriff. That is not nothing. In Lorain County, that is rare.

It is also why credit matters. This moment exists because Garon Petty refused to let the issue be waved away. He asked. He followed up. He copied oversight bodies. He persisted when dismissal would have been easier for everyone involved. And that persistence produced something tangible. It produced paper. It produced authorization. It produced a record that now constrains what the county can credibly claim next.

Accountability is not about tone. It is about trail. And this trail just got longer.

That is how accountability actually functions at the local level. It does not arrive as a press release. It arrives as an artifact. A letter. An email. A statement that cannot be unsaid. The value of investigative reporting is not that it resolves disputes in real time. It is that it freezes moments like this so they cannot be rewritten later.

This is also why this audit comment cannot be separated from the broader body of county reporting. The same institutions that now claim openness have previously resisted audits, disputed accounting narratives, and delayed or denied public records until compelled otherwise. Readers who have followed that reporting understand what is at stake here. An audit that proceeds fully would mark a meaningful departure from past behavior. An audit that stalls, narrows, or quietly disappears would confirm the pattern yet again.

Either way, the county no longer controls the frame. The invitation has been issued. The scope has been named. The expectation has been set. What happens next will be measured against what was promised, not against what is later rationalized.

This is why the email matters. Not because it solves the problem, but because it eliminates plausible deniability. It establishes that county leadership knew scrutiny was appropriate at this moment in time. From here forward, the question is not whether oversight was demanded unfairly. The question is whether Lorain County will honor its own words.

The records will answer that. And when they do, this moment will still be here, preserved in the public record, waiting to be compared to what followed. That is the through line in this story and in so many others like it. Accountability is not about tone. It is about trail. And this trail just got longer.

Preserving the Record

This correspondence is being issued in the context of multiple, ongoing public accountability matters involving Lorain County governance, fiscal oversight, and the handling of evidence by public offices. The positions taken by the Sheriff’s Office in this matter, including assertions regarding the nonexistence of records while investigative activity proceeded, will be evaluated alongside contemporaneous statements, public communications, and official acknowledgments made elsewhere by county officials concerning audits, oversight, and institutional accountability.

Nothing in this letter should be construed as isolated from that broader record. To the contrary, this matter will be assessed in light of the totality of Lorain County’s representations, actions, and documented positions regarding transparency and review. The preservation of that context is intentional.

Legal, Editorial, and Transparency Disclosures

This article is published by Aaron Knapp in his capacity as an investigative journalist and commentator and reflects reporting, analysis, and opinion based on publicly available records, contemporaneous communications, firsthand knowledge, and documented interactions with public officials. Any factual assertions are intended to be grounded in verifiable sources or direct personal experience. Readers are encouraged to review original source documents where available and to draw their own conclusions.

Nothing in this publication constitutes legal advice. This article does not create an attorney client relationship, does not offer guidance on any specific legal matter, and should not be relied upon as a substitute for consultation with a licensed attorney. Individuals or entities seeking legal advice should consult counsel of their choosing.

All individuals referenced in this reporting are presumed innocent of any wrongdoing unless and until proven otherwise in a court of law. Allegations, disputes, and conflicts described herein are reported as matters of public record, public concern, or ongoing inquiry and are presented for the purpose of accountability journalism, not adjudication.

This reporting is published in good faith. If a material factual error is identified, a correction will be considered and, where appropriate, published. Readers with relevant documentation that clarifies or contradicts any point raised are invited to submit that information for review.

Use of Images and Artificial Intelligence

Some images used in connection with this publication may be illustrative, editorial, or symbolic in nature and may include images generated or enhanced using artificial intelligence tools. Such images are not intended to depict actual events, persons, or locations unless explicitly stated. AI generated images are used for visual context only and are clearly distinguished from documentary photographs when applicable.

Business Entity Disclosure

This publication is produced and distributed by Knapp Unplugged Media LLC, an Ohio registered limited liability company, doing business as Unplugged with Aaron Knapp. Content published under this name represents independent journalism and commentary. No government entity, political campaign, or public office exercises editorial control over this work.

Recent Lorain County Reporting

A Filing the Lorain County Commissioners Did Not Want the Public to Read — A federal brief that shifted control of a long-running dispute by putting Commissioners’ arguments on the docket instead of behind press releases.

https://aaronknappunplugged.com/news/a-filing-the-lorain-county-commissioners-did-not-want-the-public-to-read/

“Their Decisions Have Put the Lorain County Population at Risk” — A direct examination of the threatened repossession of 41 sheriff’s cruisers and what it reveals about fiscal mismanagement, public-safety risk, and the consequences of county budgeting decisions.

https://aaronknappunplugged.com/news/their-decisions-have-put-the-lorain-county-population-at-risk/

Other Significant County Reports (Commissioners Tag Archive)

These stories are tagged for Lorain County Commissioners on your site and are central to contextualizing patterns of governance, transparency resistance, and public records disputes:

The Barilla Judgment and What the Court Actually Found — How a public records mandamus case exposed systemic resistance to disclosure and tied legal liability to delay and withholding.

https://aaronknappunplugged.com/news/the-barilla-judgment-and-what-the-court-actually-found/

A Manufactured Headline Masquerading as Relief — A critique of messaging from county leadership when faced with governance controversy.

https://aaronknappunplugged.com/news/a-manufactured-headline-masquerading-as-relief/

Additional County Finance & Accountability Pieces You May Link

The following reports connect to the broader financial context of Lorain County that underpins this audit discussion:

What a $125 Million Payroll Leaves Behind — A detailed analysis of the county’s largest recurring expense and the transparency issues that surrounded its release.

https://aaronknappunplugged.com/news/what-a-125-million-payroll-leaves-behind/

The Warning That Preceded the Collapse — Reporting on institutional knowledge before significant fiscal or operational breakdowns.

https://aaronknappunplugged.com/news/the-warning-that-preceded-the-collapse/